Section 754 Elections in Tiered Partnership Structures

- Published

- Jun 8, 2026

- Share

You’ve just purchased a partnership interest from an existing partner and are expecting additional depreciation. Or, perhaps, you’ve inherited a partnership interest and looking to reap some of the benefits of that increase in value without selling your interest. A Section 754 election can help you take advantage of any potential benefits.

Key Takeaways

- A Section 754 election lets a partnership step up the basis of its assets to align inside basis with outside basis after a partner buys in, redeems, or inherits an interest.

- The election triggers a Section 743(b) adjustment when an interest transfers by sale, exchange, or death, and a Section 734(b) adjustment when the partnership redeems an interest with cash or property.

- The partnership makes the election by attaching a written statement to a timely filed return (including extensions); once made, the election applies to all subsequent years and is generally irrevocable.

- In a tiered structure, additional depreciation deductions flow through only when both the upper-tier and lower-tier partnerships have a valid Section 754 election in effect.

- Revenue Ruling 87-115 governs the interaction between tiers: if only the upper-tier partnership elects, the basis adjustment is limited to its interest in the lower-tier partnership; if only the lower-tier partnership elects, no adjustment occurs at either tier.

- Without consistent elections at every tier, a new or successor partner may not claim current depreciation deductions and will only recover the additional basis on a future sale or disposition.

What is a Section 754 Election?

A Section 754 election allows a partnership to elect to increase, or step up, the basis of the assets within the partnership. The step-up is used to equate, for tax purposes, the partner’s basis in its interest in the partnership (i.e., outside basis) to the partnership’s basis in its assets (i.e., inside basis). The election is available for both a distribution of partnership property or a transfer of an interest by a partner (by sale/exchange or death).

When a partnership purchases an interest from a partner (i.e., distributes cash and/or property in redemption of the partner’s interest) in a taxable transaction, the step-up is allocable to all partners and is reported on the partnership’s balance sheet. This is known as a Section 734(b) basis adjustment.

By contrast, where there is a taxable sale/exchange of a partnership’s interest or transfer to a decedent’s estate due to the partner’s death, the step-up is allocable only to the new partner. This is known as a Section 743(b) basis adjustment.

The election and corresponding Section 734(b) or 743(b) basis adjustment are made by the partnership by attaching a written statement, which includes calculations of the step-up, with a timely filed (including extensions) tax return. The election is in effect for the year filed and any subsequent years. It is generally irrevocable, although it can be revoked, in extremely limited circumstances, with IRS consent.

How Does a Section 754 Election Work in Tiered Partnerships?

What happens when the Section 754 election is made at an upper-tier partnership and the underlying asset/property is two or more tiers below?

Example - John is acquiring Bob’s partnership interest in ABC LLC for $100,000. Bob’s basis in the partnership is $25,0000. ABC LLC owns a partnership interest in Blackacre LLC, which owns a property, Blackacre. John would like to make use of the $75,000 of additional basis through allocations of additional depreciation deductions.

For a partner in an upper-tier partnership to benefit from these additional depreciation deductions, in addition to making the Section 754 election at the upper-tier level, additional elections/rules have to be followed.

When Must Both Tiers Make a Section 754 Election?

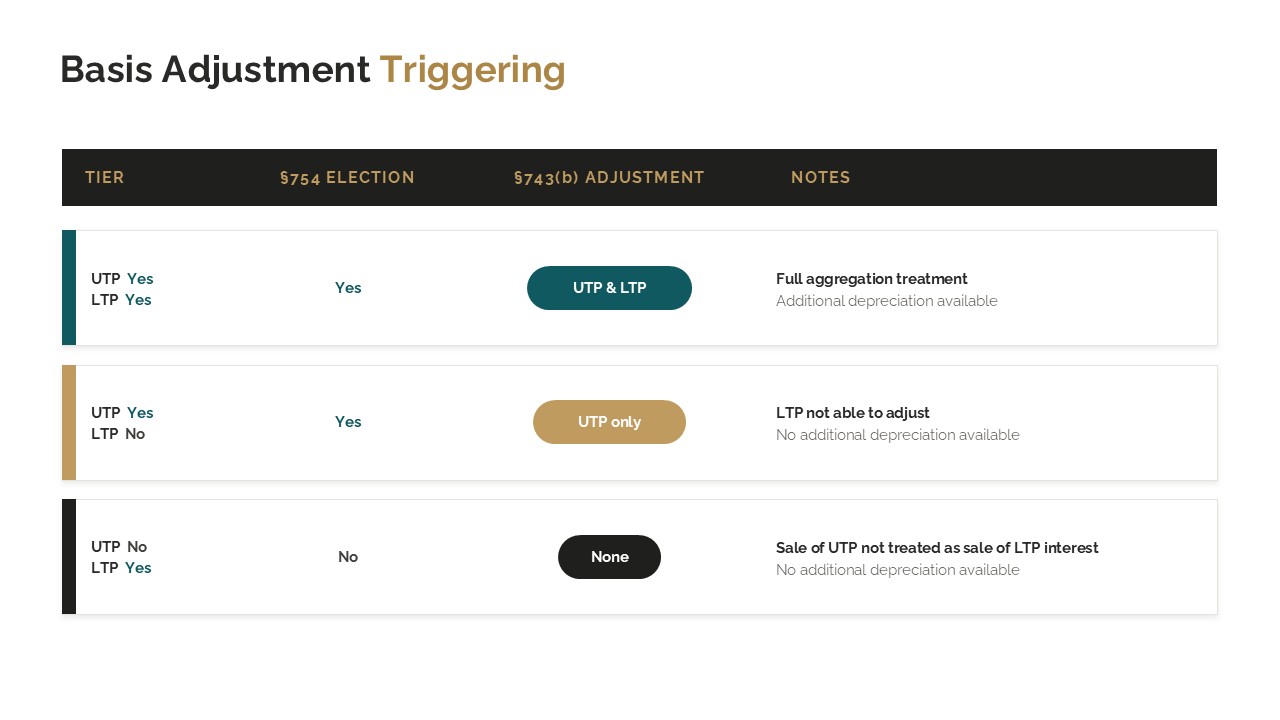

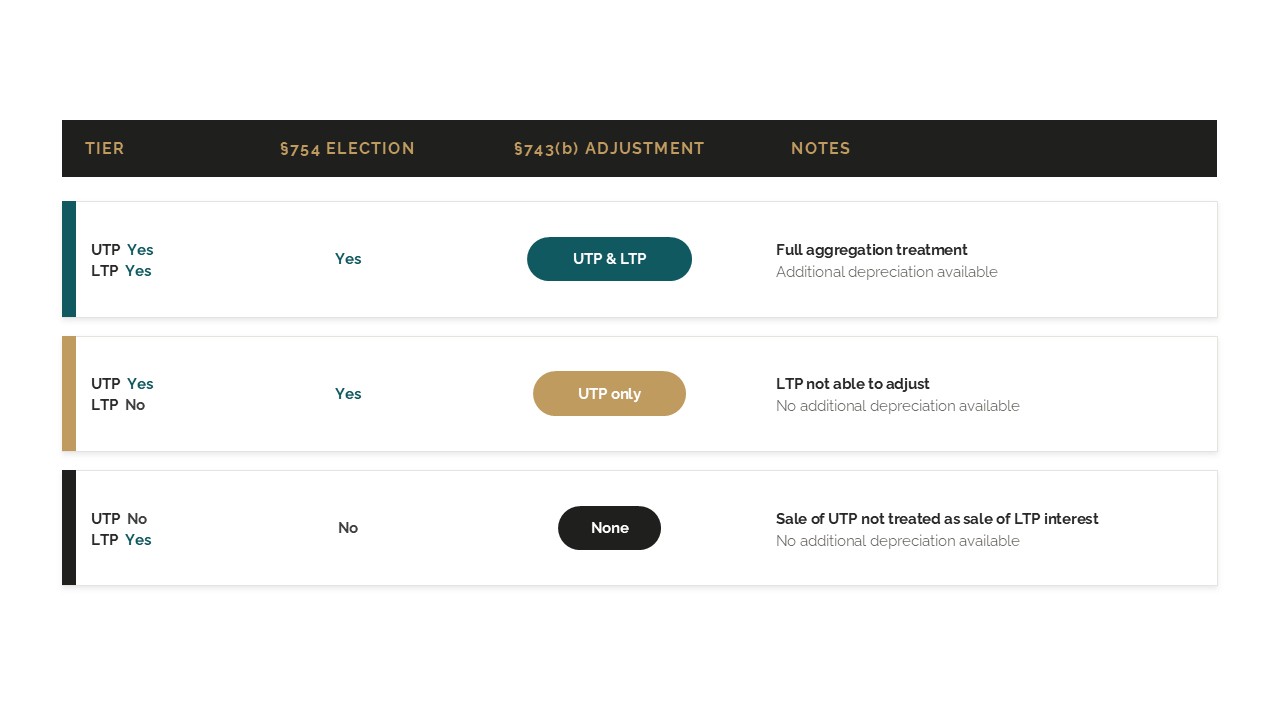

Revenue Ruling 87-115 addresses the application of the optional basis adjustment election under Section 754 in a tiered partnership structure, where an upper-tier partnership (“UTP”) holds an interest in a lower-tier partnership (“LTP”) that holds property. The results depend on whether both the UTP and LTP make a Section 754 election, only the UTP makes the election or only the LTP makes the election.

When a partner in the UTP sells or exchanges its UTP interest, or a transfer upon death occurs, and both UTP and LTP have made valid Section 754 elections, the sale/transfer is treated as if the interests in the underlying LTP are sold as well. The UTP computes an adjustment for its interest in the LTP and the LTP makes a corresponding adjustment in its assets, aligning bases.

In tiered partnerships, confusion can arise because both the UTP and the LTP may be treated as separate partnerships for Section 754 purposes. If only the UTP has the Section 754 election in effect and the LTP does not, the LTP cannot make its own adjustment. Only the UTP will make an adjustment in this case, in the basis in its interest in the LTP. Conversely, if only the LTP has the Section 754 election in effect, then the sale of the UTP interest will not trigger an adjustment for either tier, since the UTP’s lack of election indicates separate entity treatment for each partnership rather than aggregate treatment.

Continuing the above example, there is $75,000 of additional basis because of John’s purchase. In order to claim additional depreciation deductions, , both the LTP (Blackacre LLC) and UTP (ABC LLC) must make a Section 754 election. Absent the elections, John will only benefit upon sale or disposition of his interest (i.e., additional basis to offset any gain on sale).

Revenue Ruling 87-115 also describes the rules for the allocation of the additional basis adjustment between capital and non-capital assets of the partnership. In the example above, there is only one asset and the entire basis adjustment is allocable to this asset.

The ruling provides clear guidance for multi-tier partnerships when basis adjustments should be made and how the elections at each tier determine the outcome. Without consistent Section 754 elections, the tax basis of assets may not properly reflect changes in ownership and can lead to potential variances in gain or loss recognition as well as an inability to take current depreciation deductions. These key points are critical for tax planning, especially in real estate ownership structures where tiered partnerships are common.

Planning a Partnership Transfer in a Tiered Structure?

A Section 754 election sounds straightforward until the structure has two or more tiers. Getting it right requires coordinated elections, careful basis calculations, and a clear view of how Revenue Ruling 87-115 applies to your facts.

EisnerAmper's Real Estate teams help partners and partnerships work through these decisions before a transfer closes, when the planning options are widest. Contact us to discuss your structure.

What's on Your Mind?

David Rackman

David Rackman is a Partner and a member of the firm's Real Estate Private Equity Group with extensive experience in partnership tax, providing compliance, planning, and advisory services to high-net-worth individuals and families.

Start a conversation with David