Valuing Ownership Interests in Multi-Tiered Entities

- Published

- Mar 24, 2026

- Share

Key Takeaway:

Ownership interests in multi-tiered entities, structures where an entity holds an ownership interest in one or more other entities, are commonly valued for estate or gift tax planning purposes. These structures can present unique considerations for the valuation appraiser, especially in the application of valuation discounts.

When preparing valuations for tax purposes, such as those prepared for estate or gift tax planning purposes, valuation professionals often determine the value of an ownership interest in a multi-tiered entity. Multi-tiered entities are created with consideration given to their favorable tax and legal attributes. These structures afford the ability to incorporate multiple layers of ownership and control, which can present unique considerations when performing a valuation of an ownership interest within the structure.

Defining a Multi-Tiered Entity

A multi-tiered entity consists of an entity that holds an ownership interest in one or more other entities. These structures can often include holding companies that own tangible assets such as real estate or fine art, as well as other assets such as securities and investments.

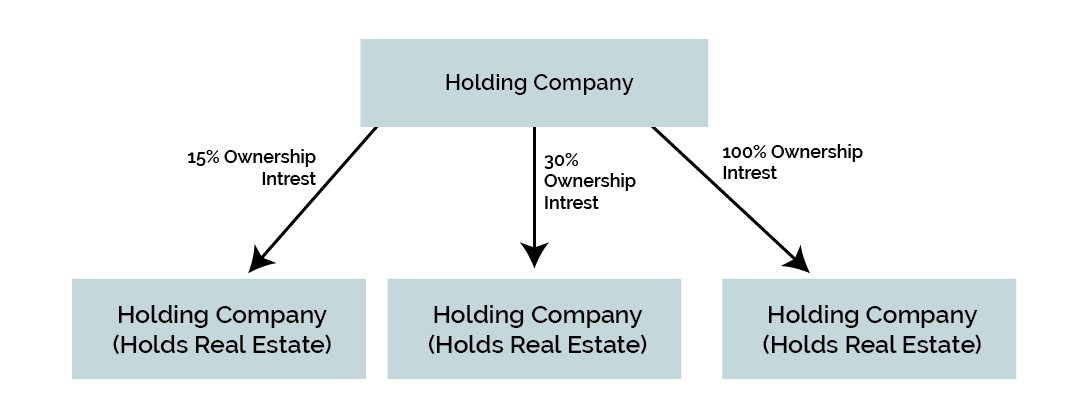

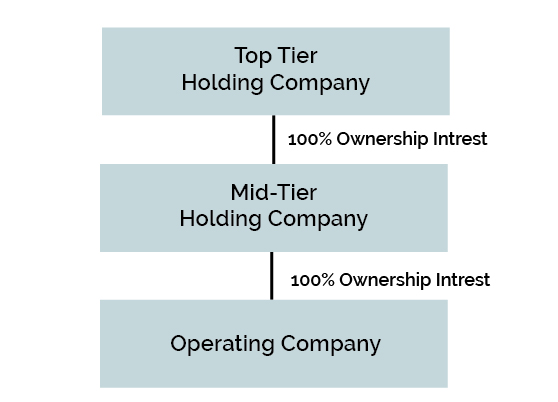

A multi-tiered entity may also consist of a holding company that directly, or indirectly through other entities, holds an ownership interest in an operating company. Ownership interests held within a multi-tiered entity structure can be wholly-owned (100%) or partially owned (less than 100%), or the structure may contain a mix of both types of ownership.

The following diagrams show two illustrative examples of multi-tiered entities.

The Importance of Understanding an Entity’s Structure

Multi-tiered entities can be complex in nature, and it is critical to understand the structure and the attributes of each entity in the structure. Prior to commencing the valuation process, the following documents and information should be obtained:

- An organizational chart with all entities in the structure, including owners and the corresponding percentage ownership interest in each entity.

- Governing documents, such as limited liability, company agreements, or operating agreements, for each entity in the structure to understand key provisions regarding the rights and restrictions afforded owners of each entity.

- Financial statements for each entity in the structure.

- Market values for tangible assets such as real estate or fine art from third-party appraisers with experience in valuing those specific types of assets.

- Market values for securities or investments based on brokerage statements or net asset value (NAV) statements, to the extent available.

Approaches to Valuing Multi-Tiered Entities

In determining the value of an ownership interest in a multi-tiered entity, the value of each entity in the structure must be determined.

The most commonly used approach to value holding companies is the asset-based approach, which determines an entity’s adjusted net asset value (with net asset value defined as total assets less total liabilities) by adjusting the values of an entity’s assets and liabilities from its book values to market values. For valuing operating companies, the market and income approaches are most commonly used.

For holding companies, the valuation of certain tangible assets such as real estate may incorporate the market approach or income approach to determine market value. Securities or investments are typically valued using the asset-based approach, with market value based on NAV, which is typically valued considering the cost (asset-based), income and market approaches.

Considerations for Applying Valuation Discounts

Understanding the ownership interest to be valued at each entity level within the structure is critical to a proper analysis. The appraiser must understand whether the ownership interest at each entity level is controlling or non-controlling, and marketable or non-marketable. These attributes impact what valuation discounts are applicable, and at which levels within the structure. The most commonly applied discounts in valuation are a discount for lack of control (DLOC) and a discount for lack of marketability (DLOM).

A discount for lack of control is applied to the value of an entity to reflect that the holder of a non-controlling interest in that entity lacks the ability to exert control over the entity due to the size or attributes of the ownership interest.

A discount for lack of marketability is applied to the value of an entity to reflect an owner’s inability to sell a non-controlling ownership interest in an entity for which there is no ready market where it may be converted to cash, unlike holders of stock in publicly-registered securities in active, liquid markets. The DLOM considers the rights and restrictions afforded an ownership interest in an entity, such as distributions, transferability, and management of the entity.

The magnitude of discounts applied are based upon the characteristics and attributes of each entity and the ownership interest being valued, with consideration given to governance, financial performance and the risk characteristics of the assets held by the entity, among others.

An important consideration for valuation discounts specific to multi-tiered entities is that the appraiser must consider the aggregate effect of discounts applied at different entity levels within the structure, in order to avoid double-counting specific attributes or risks that may exist at multiple levels within the structure.

Concluding Thoughts

Multi-tiered entities present unique considerations for the valuation appraiser. Key amongst those considerations are a thorough understanding of the entity’s structure, which enables the appraiser to thoughtfully apply valuation discounts at the appropriate levels of the structure.

What's on Your Mind?

Nicole S. Podendorf

Nicole Podendorf is a Director in the Corporate Finance Group, specializing in business valuation, complex commercial litigation and forensic investigations and consults on specific valuation issues.

Start a conversation with Nicole