The Why, How and When of Fraud Detection

- Published

- Nov 17, 2019

- By

- Hubert Klein

- Share

The Association of Certified Fraud Examiners (“ACFE”) defines occupational fraud as “the use of one’s occupation for personal enrichment through the deliberate misuse or misapplication of the organization’s resources or assets.” The ACFE’s 2018 Global Study on Occupational Fraud and Abuse shows that occupational fraud continues to plague businesses both domestically and internationally.

No business is immune from fraud. As such, it is highly recommended to perform regular fraud risk assessments. This is not a one-size-fits-all review. Each company is unique based on its size, location, industry and available resources. As in any business, there are risks; the risk of occupational fraud is no different. From an organizational standpoint, the questions become how much risk is your organization willing to take, and what can the business do to minimize those risks? All of this should be considered when identifying areas susceptible to fraud and prioritizing where to implement resources to prevent and detect fraud.

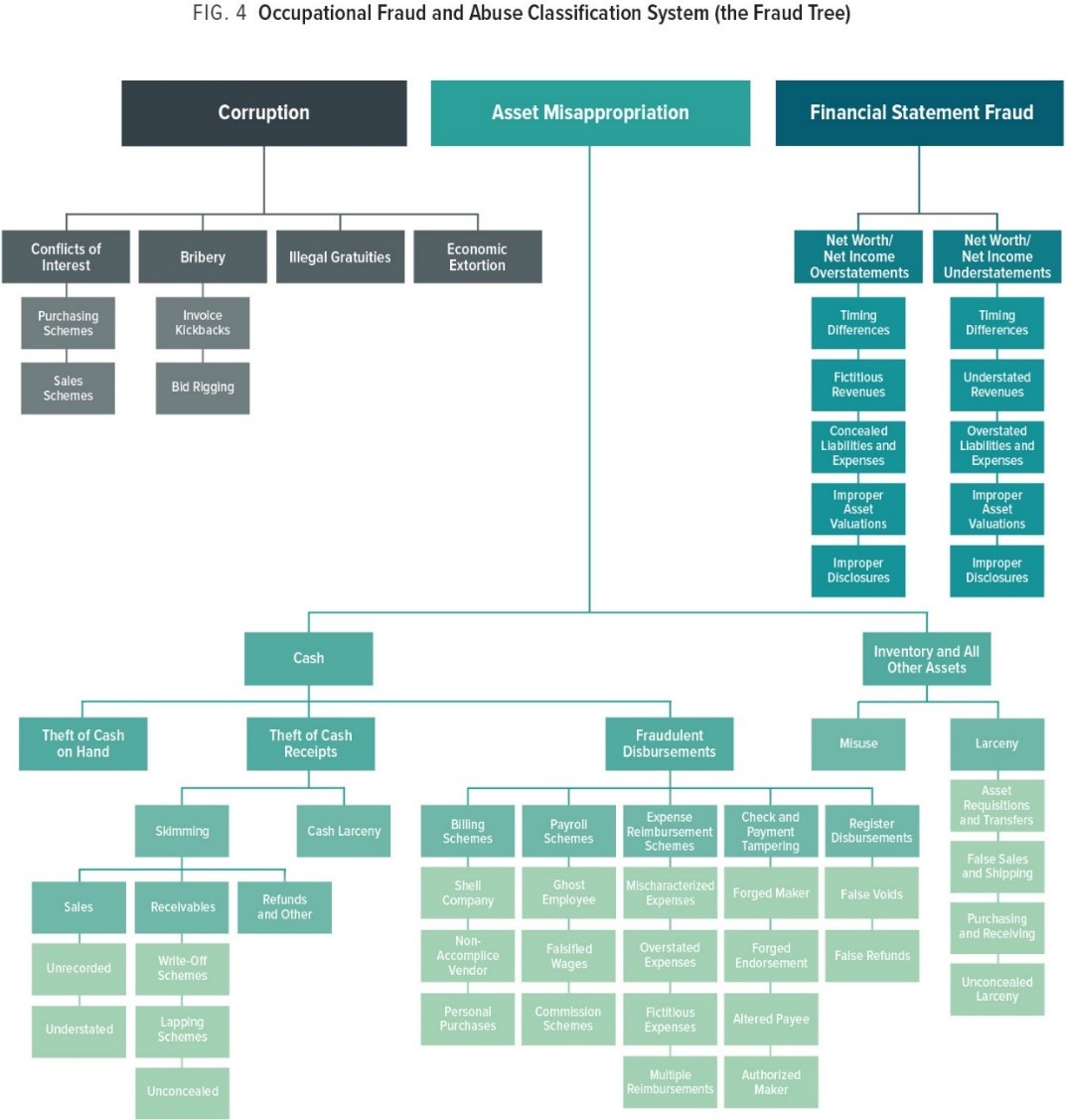

The ACFE has developed an Occupational Fraud and Abuse Classification System, also known as the Fraud Tree (Fig. 4). This exhibit provides common fraud types and is a great place to start when assessing your company’s risk.

You want to believe that your company has the best employees. They might feel like family, and you might think they would never steal from you. However, how well do you know the person sitting next to you? What are they struggling with? Can they justify to themselves taking just enough to cover this week’s bills? If you cannot answer with 100% assurance that your employees are under no pressure and there is no opportunity for them to help themselves to the organization’s resources or assets, then you have the potential for fraud.

Studies show that there is a paradigm known as the fraud triangle. It consists of three key elements that need be present for a fraudster to commit a wrongful act: (1) pressure; (2) opportunity; and (3) rationalization. In occupational fraud schemes, perpetrators are generally under pressure and do not feel that their problems can be shared. The opportunity exists when they see a way to relieve the pressure and believe they won’t get caught. Finally, fraudsters will rationalize that they are doing the wrong thing, however, for the right reasons.

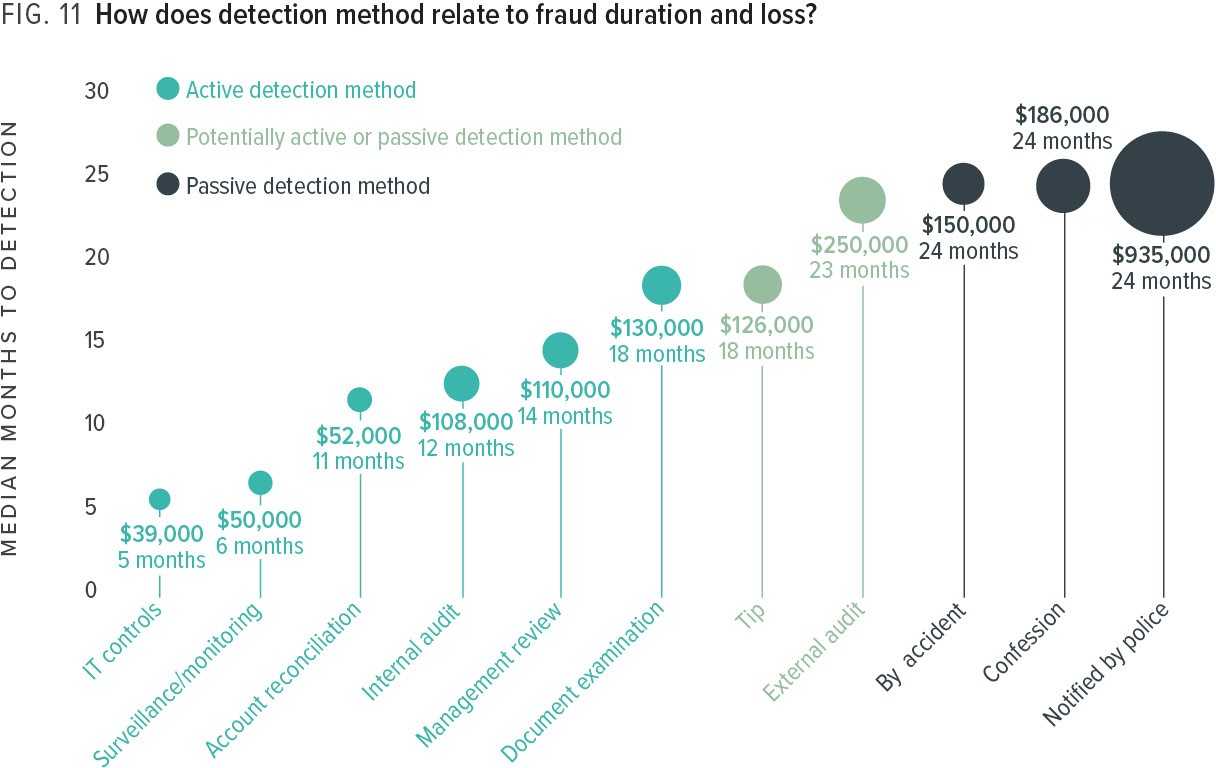

So how does your company stop fraud? Just increasing the perception of fraud detection can be an effective prevention method. The ACFE survey revealed that the method in which the fraud is uncovered could vastly influence the effect the fraud has on the company (Fig. 11). Active detection methods or controls designed to detect fraud are typically cheaper and tend to detect fraud more quickly. For instance, if a surveillance camera (active detection) caught an employee stealing from a cash register, the issue would be resolved quickly with substantial evidence of wrongdoing and minimal losses to the company. However, having few or no detection methods in place and relying on luck or confessions can result in ongoing instances of fraud, leading to substantial losses.

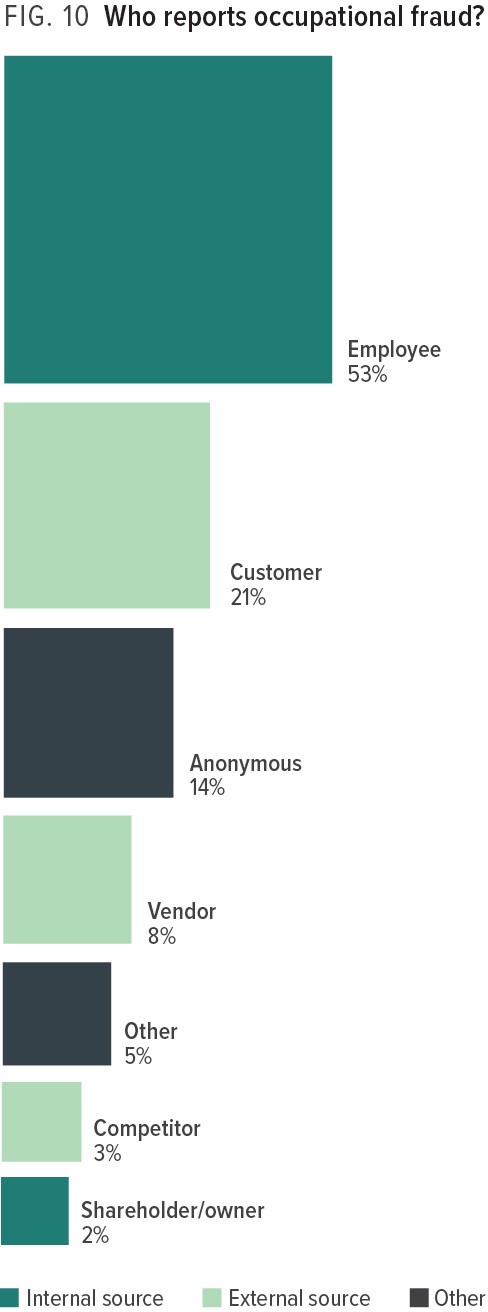

One of the most successful detection methods a company can implement is the use of a tip hotline (active detection). Contrary to what most people might think, the majority of occupational fraud schemes are not detected as a result of the work performed by internal or external auditors. Instead, they are usually uncovered through tips—40% of the cases cited in the ACFE’s survey. These tips usually come from other employees within the organization, but it is not uncommon for people outside of the organization (e.g., customers, vendors, shareholders, even competitors) to leave a helpful tip. The ACFE graph below illustrates those who are reporting the frauds.

One major issue for anyone reporting a suspected instance of occupational fraud is to whom should the report be made once fraud is suspected and/or uncovered? Most people tend to communicate information to their direct supervisor. Depending on the department in which the fraud is uncovered, the organizational level of the employee committing the fraud, and other variables involved, it may (or may not) be appropriate to relay the information to a direct supervisor.

Companies have taken notice of this and begun to implement procedures for those who would like to report suspected instances of occupational fraud through tip hotlines. These hotlines can be either internal or external through a private company or fraud-fighting organization. Many companies have developed policies and procedures for where and how to report tips for suspected fraud activity.

The longer occupational fraud continues, the greater the financial loss. Knowing how occupational frauds occur and are detected and reported is important, because it helps when designing and strengthening an organization’s fraud-fighting controls. It is also useful when designing, reviewing and updating organizational policies and procedures as they relate to the detection of occupational fraud within an organization. Organizations that are proactive can substantially reduce their risk of occupational fraud and financial loss.

FRAUD WEEK

ARTICLES

- The Why, How and When of Fraud Detection

- A Roadmap for Preventing Expense Reimbursement Fraud

- Combatting Grant Fraud in Not-for-Profits

- To Trust or Not to Trust the Trustee?

- When You’re in the Eye of the Shareholder Dispute Storm

- Breaking Up Is Hard to Do: Business Valuation in Owner Disputes

BLOGS

What's on Your Mind?

Hubert Klein

Hubert Klein a Partner, the Firmwide Valuation Services Leader, and the New Jersey Forensic, Litigation & Valuation Services (“FLVS”) Market Leader, is a nationally recognized expert witness and professional educator in forensic accounting, damages, and valuation topics.

Start a conversation with Hubert