Selected Taxation Case Studies of 2019 NBA Free Agent and Rookie Signings

- Published

- Jun 28, 2019

- Share

This analysis will show the impact of where selected NBA players play their home games. For illustrative purposes, we have calculated the tax consequences of Zion Williamson being a member of the New Orleans Pelicans; Kevin Durant signing with the Golden State Warriors, New York Knicks and Brooklyn Nets; and Kawhi Leonard signing with the Toronto Raptors, New York Knicks, Brooklyn Nets and either of the Los Angeles teams.

This analysis assumes that each player would be a resident of the state and city where their team plays their home games, with the exception of Kawhi Leonard possibly re-signing with the Raptors. For that illustration, we assume that Kawhi is a non-resident of Canada (see below). It does not factor in incremental tax for playing games in non-resident states with a higher tax rate since that would be insignificant for this illustration.

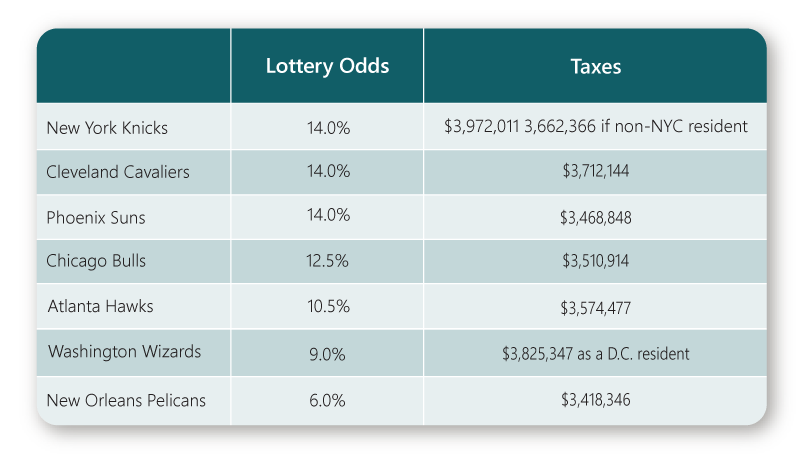

Zion Williamson

The Duke University standout was selected by the New Orleans Pelicans with the No. 1 pick in the 2019 NBA Draft.

From a tax perspective, Zion landed at the optimum destination since Louisiana has the lowest state income tax rate of the franchises that had a high probability of winning the first pick! Below are Zion’s projected tax liabilities as a Louisiana resident as well as for the other states.

Example

- $8 million estimated wages during the 2020 tax year.

- Estimated taxes below include federal, state and city.

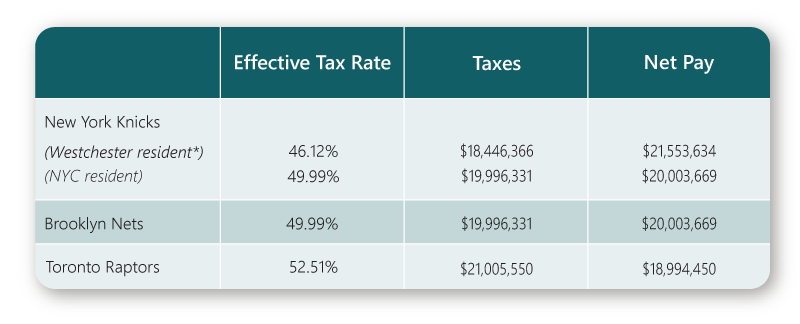

Kevin Durant (“KD”)

The two-time NBA finals MVP and NBA champion (2017, 2018) may enter NBA free agency on June 30 if he elects to decline his $31.5 million player option. Injured during the 2019 NBA Playoffs, he will need to consider several factors such as health, family life, location, team culture, team medical staff, business opportunities and, of course, taxes. Teams will need to consider if they want to sign KD to a long-term max contract given his age and the fact that he may miss the entire 2019-2020 season.

Rich Kleiman, KD’s sports agent and business partner, will be providing as much information as possible in order for KD to choose the optimal destination. According to ESPN’s Stephen A. Smith, the Golden State Warriors, Brooklyn Nets and New York Knicks are currently the frontrunners. Here are KD’s projected tax liabilities for signing with these franchises.

Example

- $40 million estimated wages during the 2020 tax year.

- Estimated taxes below include federal, state and city.

- Example does not include estimated taxes on endorsements.

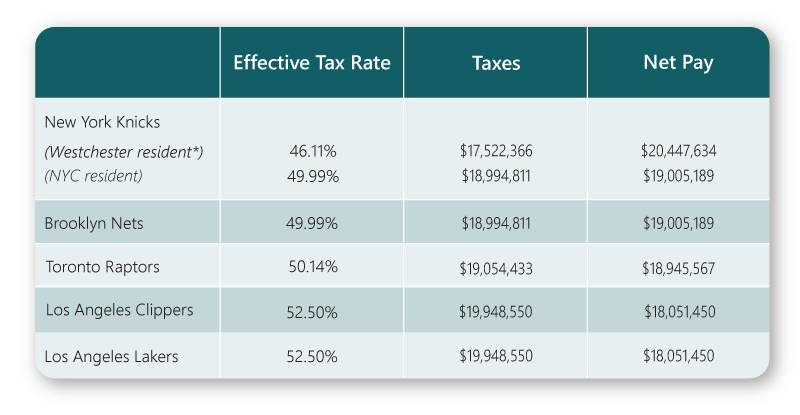

Kawhi Leonard

Another two-time NBA finals MVP and NBA champion (2014, 2019), Kawhi enters NBA free agency on June 30.

According to NFL Hall of Famer and Fox Sports analyst Cris Carter, Kawhi is focusing on five potential suitors during this pre-free agency period. The five, in no particular order, are the Los Angeles Clippers, Los Angeles Lakers, Toronto Raptors, New York Knicks and Brooklyn Nets. See example below for Kawhi’s projected tax liabilities should he choose one of these franchises.

Example

- $38 million estimated wages during the 2020 tax year.

- Estimated taxes below include federal, state, city and province.

- Example does not include estimated taxes on endorsements.

- Assumes Kawhi remains a resident of the United States, and wages from Raptors are sourced 66% to Canada.

*The New York Knicks’ practice facility is in Westchester County, NY.

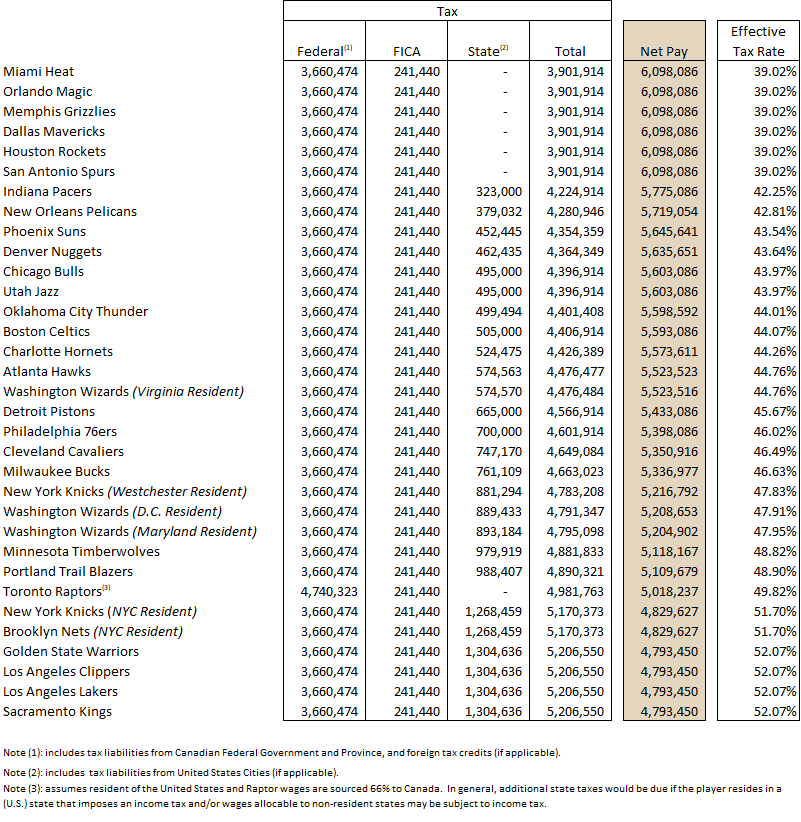

NBA Franchises’ Tax Liabilities

Here are the projected federal, state, and local tax liabilities, including FICA and Medicare tax, for an NBA free agent signing a $10 million contract for the 2019-2020 season. The chart also includes net pay and the aggregate rate of tax.

Other Considerations

There are a variety of other factors at play when it comes to a professional athlete choosing a new team. The key consideration is residency. Most athletes choose to establish domicile in Florida, Texas or Nevada – states where there are no state income taxes. However, athletes need to be wary of the statutory residency trap where states will tax you as a full-year resident if you meet certain presence tests.

For those athletes living in a state with an income tax, they will receive a credit for taxes paid to other states where they perform. In general, the credit is limited to double-taxed source income; and players may be subject to an incremental state tax on the income allocated to a state with a higher tax rate.

Bonuses received for signing a contract are not subject to allocation if the bonus is not contingent on playing any games, payable separate from salary, and nonrefundable. Thus, there is a huge benefit to residing in a state without an income tax and signing a contract in your home state; the bonus would not be subject to any state income tax.

Athletes allocate compensation, including playoff shares and performance bonus, based on a “duty day” formula. Duty days include all contractual pre-season training periods through the last game in which the team competes.

Appearance fees are also subject to tax in the states where services are performed. There are no explicit guidelines detailing the allocation of income received from endorsements, but case law suggests that it is allocable based on the geographical location of promotional appearances and where advice and consultation is provided.

Given the complexities of contracts, signing bonuses, residency and a myriad of other issues, it is strongly recommended that owners, sports agents, and athletes consult with their tax advisors for a full tax analysis.

What's on Your Mind?

James A. Jacaruso, Jr.

James A. Jacaruso Jr. is a Private Client Services Group Director with more than 25 years of tax compliance and planning experience focusing on personal and fiduciary income taxation, gift taxation and wealth transfer planning.

Start a conversation with James