ASC Topic 606: Contract Assets and Liabilities for the Construction Industry

- Published

- Jan 29, 2024

- Share

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 606, Revenue from Contracts with Customers (“ASC 606”), has brought with it new qualitative and quantitative disclosure requirements for entities issuing financial statements in many industries, including construction. ASC 606 provides a more comprehensive framework for addressing revenue issues and establishes enhanced disclosure requirements to provide financial statement users with more detailed information about the nature, timing, and uncertainty of revenue from contracts with customers.

What are contract assets and liabilities under ASC 606?

One of the biggest impacts ASC 606 has brought to contractors is the re-definition of contract assets and liabilities and their presentation and disclosure within the financial statements and footnotes.

Under ASC 606, contract assets and liabilities are accumulated and presented on a net basis from the individual contract level. ASC 606 states that a contract asset arises as an entity’s right to consideration in exchange for goods or services that the entity has transferred to a customer when that right is conditioned on something other than the passage of time. Contract assets include:

- Costs and estimated earnings in excess of billings on uncompleted contracts (i.e., unbilled receivables)

- Retainage receivables

- Uninstalled materials

Contract liabilities represent an entity’s obligation to transfer goods or services to a customer. Examples include:

- Billings in excess of costs and earnings (i.e., deferred or unearned revenue), net of conditional retainage receivable

- Retainage payables

Retainage classification: Receivable/payable vs. contract asset/liability

In the area of retainage, differs from legacy generally accepted accounting principles (“GAAP”). Under legacy GAAP, retainage receivables were presented and disclosed with contract receivables, and retainage payables were presented and disclosed with contract payables. ASC 606 defines a receivable as an entity’s right to consideration that is unconditional, albeit only the passage of time is required before payment of that consideration is due.

In the construction industry, retention provisions in construction contracts are a common form of security where the customer withholds a portion of the consideration billed by the contractor as the contractor completes their work appropriately and in accordance with the contract terms and specifications. Generally, payment of retainage is subject to the completion of future obligations under the contract, such as meeting certain milestones. This is known as conditional retainage. Careful evaluation of the correct classification of retainage is critical to the proper accounting treatment, presentation, and disclosure of these items.

Conditional retainage should be included in the contract asset (or contract liability) and determined at the individual contract level. At each reporting date, issuers accumulate their contract assets and liabilities under their balance sheet accounts, separating and presenting between current and noncurrent amounts as per the entity’s accounting policies and operating cycle.

Applying these new definitions and classifications under ASC 606 requires reporting companies to revise their footnote disclosures to the financial statements in the following areas:

- Significant accounting policies footnote (revisions to re-definition of contract receivables, contract assets, and contract liabilities)

- Contract assets and liabilities disclosure

- Supplemental schedule of contract information changes

All construction contractors should disclose and present separately on the face of the balance sheet the opening and closing balances of contract receivables, payables, contract assets, and contract liabilities. There is some flexibility with how to present and disclose within the financial statement footnotes the contract receivables, payables, contract assets, contract liabilities, and supplemental information in accordance with ASC 606.

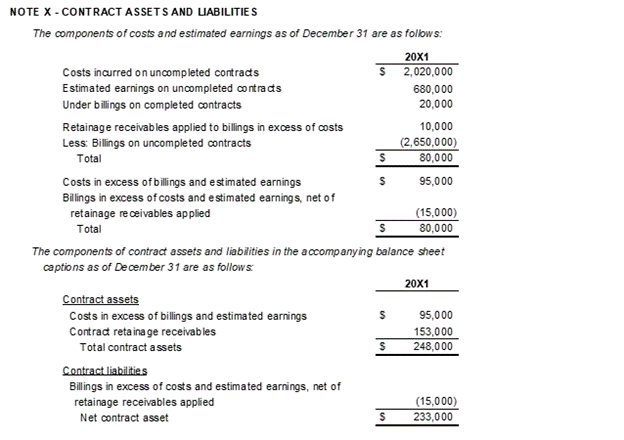

The following examples are options to consider in providing the desired information for financial statement users in the construction industry.

Understanding the impacts of correct classification

Classification of contract assets, liabilities, and retainage may impact performance metrics, debt covenants, borrowing base determinations, or financial ratios included in the company’s financial statements. Reviewing such financial statement classifications is important to determine how the classification of these affects the company’s ability to meet its financial covenants.

- Does Your Construction Company Qualify for the Research and Development Credit?

- Inflation Reduction Act: Tax Provisions for Business Owners

- Clean Energy Tax Credits in the Inflation Reduction Act

- Inflation Reduction Act Updates to the IRC Sec. 45L Tax Credit

- Contract Assets and Liabilities Within the Scope of ASC Topic 606 for the Construction Industry

Contact EisnerAmper

Ready to take the next step? Share your information and we’ll reach out to discuss how we can help.