Family Office Conference

- Published

- Nov 28, 2022

- Share

On November 15, EisnerAmper partnered with Dentons Family Office team and Silicon Valley Private Bank to host a Family Office Conference in West Palm Beach, Florida. Items of interest to family offices including mid-term and future elections, policy proposals/changes and tax strategies were discussed in depth by the panelists. Below is a summary of the EisnerAmper portion of the presentation.

One of our Managing Directors, moderated the EisnerAmper panel. The panelists included:

- Patrick Mangan, Partner, Private Client Services

- Lisa Cappiello, Director, Private Client Services

Methods of tax-deferral and elimination:

IRC Sec. 1031 Exchanges: An IRC Sec. 1031 exchange is an effective method for investors to defer taxable income from the sale of investment property by reinvesting the proceeds into like-kind property of equal or greater value. Lisa touched on some of the rules and concepts surrounding the IRC Sec. 1031 tax-deferred exchange procedure. Generally, an investor must identify the replacement property within 45 days of the sale of assets and complete the exchange within 180 days. All capital improvements and construction intended to be included in the exchange must be completed within the 180-day timeframe to qualify as part of the exchange.

Qualified Opportunity Zones: Established by the 2017 Tax Cuts and Jobs Act (TCJA), qualified opportunity zones (QOZs) result from an economic development program designed to encourage investment into distressed communities throughout the United States. The QOZ program offers investors an opportunity to defer and potentially reduce capital gains tax while participating in the program. To qualify for capital gain tax deferral, a taxpayer must invest the proceeds from the realized capital gain into a qualified opportunity fund (QOF) within 180 days from the sale of the appreciated asset. Contrary to IRC Sec. 1031 exchanges, qualified assets are not limited to like-kind property and may include gains from sale of stocks and other securities or property.

Taxpayers can defer capital gains invested in QOFs through December 31, 2026, or until the interest in the QOF is sold or exchanged. Additional tax incentives such as a 10% and 15% step-up in tax basis are available for taxpayers who defer gains for five and seven years respectively. Investments made by December 31, 2019, and December 31, 2021, are eligible to receive the benefit of step-up in tax basis.

Taxpayers can avoid capital gains tax on the appreciated property completely if the investment in the QOF is held for at least ten years.

QOF investments have created significant opportunities in trust and estate tax planning. An interest in a QOF can be transferred to a grantor trust or the spouse of the taxpayer without creating an inclusion event. Further, a distribution to the taxpayer’s beneficiaries upon death will also avoid an inclusion event, allowing the recipient of the QOF interest to continue to defer the built-in capital gain until December 31, 2026.

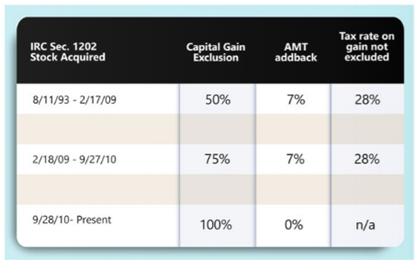

IRC Sec. 1202 Qualified Small Business Stock (QSBS): IRC Sec. 1202 was enacted to encourage investment in small business by providing tax benefits to those willing to take on the risk and uncertainty associated with early-stage companies. With certain exceptions, a QSB is a C corporation engaged in an active business with the tax basis of gross assets under $50 million. For an investor to qualify for QSBS treatment, they must acquire stock of the corporation at its original issuance and hold it for at least five years. QSBS can be held by non-corporate taxpayers such as partnerships, LLCs, trusts, individuals, and S corporations. Below is a table summarizing the current exclusion benefits based on date of acquisition, tax rates on QSBS gains that are not excluded, and AMT implications. (Note: EisnerAmper has a dedicated IRC Sec. 1202 site to assist with determining eligibility, analysis, and planning.)

Tax Deduction and Planning Techniques:

Charitable Deductions and Gifting Artwork: Investors and collectors have supported the mission of tax-exempt entities for decades through donating artwork from their collections. While the act of donating artwork supports investor’s philanthropic efforts, it also presents several tax benefits and planning opportunities.

Marie provided insights regarding tax concepts such as “investor vs. dealer,” qualified organizations, “related-use,” holding period and valuation. Marie also provided details related to the structuring of the donation to maximize tax deductions and avoid penalties when donating fractional interests of artwork.

Bonus Depreciation: Tax year 2022 marks the beginning of the end of the favorable 100% bonus depreciation provision established by TCJA. The 100% bonus depreciation is set to decrease by 20% each year from 2022 until fully phased out at the end of 2026. Even a reduction of 20% has significant impact related to larger asset purchases. Businesses may consider accelerating larger asset purchases to take advantage of bonus depreciation with uncertainty around extension of the provision.

Business Deductions for restaurant meals: In an effort to assist struggling restaurants during the COVID-19 pandemic and encourage business spending, the IRS temporarily increased the deductibility of restaurant meals from 50% to 100%. This provision is set to expire at the end of 2022.

Pass-Through Entity (“PTE”) Tax: TCJA introduced a state and local tax (SALT) cap of $10,000 per year for individuals. This was an extraordinarily low amount for high net worth individuals and those residing in states with higher tax rates. In response, there are currently 29 states that have enacted a PTE tax, and three states with proposed PTE tax bills (State Pass-Through Entity (PTE) Level Approach (aicpa.org)). This allows a pass-through entity to pay state taxes on behalf of its partners and receive a federal deduction without brushing up against the SALT cap. Every state with a PTE tax is different in its mechanics and there are many nuances regarding timing of payments, credits received, and/or income excluded. The PTE tax provides a tremendous planning opportunity to lower one’s effective tax rate significantly and has emerged as one of the most impactful tax planning strategies in recent history. Consult with your state and local tax advisor.

Estate Planning Techniques:

Estate Planning Vehicles: Patrick touched on the importance of estate planning and the vehicle(s) used in our current market environment. Given the historic inflation we have experienced, and corresponding interest rate hikes, one must be aware of the different vehicles available and their potential benefits/downsides.

A grantor retained annuity trust (GRAT) is a well-known vehicle utilized by estate planners. They are particularly beneficial in low interest rate environments. GRATs are an irrevocable trust used to transfer wealth while preserving the lifetime federal gift and estate tax exclusion. The grantor moves assets into the trust and receives an annuity payment for several years based on IRS-published monthly interest rates. The initial transfer plus interest is returned to the grantor over the life of the trust, and the remainder can be passed on to beneficiaries. In a higher interest rate environment, the rate of return required on the assets to exceed the IRS interest rate increases. This reduces the amount that can be passed on to beneficiaries and makes it much more challenging for this vehicle to be successfully implemented.

A spousal lifetime access trust (SLAT) is an increasingly popular tool and has exploded in popularity given the increase in the federal gift and estate tax exemption included in the TCJA ($12.92 million for an individual/$25.84 million for married couples in 2023). A SLAT is an irrevocable trust that is formed by one spouse to benefit the other. The SLAT is funded by the grantor spouse using their gift tax exemption. The grantor relinquishes the right to the property, but the beneficiary spouse has access. While irrevocable in nature, the donor can potentially indirectly benefit if the couple remains married. The SLAT has flexibility in structuring such that the beneficiary and children/grandchildren can take distributions.

SLATs are most beneficial for assets that are expected to appreciate, since the estate and gift tax exemption utilized is the fair value on the date of funding. This allows the assets to grow outside of the estate, and not be subject to estate tax when the donor spouse passes. This can be a fantastic tool given a couple’s circumstances because of the flexibility provided, and ability to take advantage of the increased exclusion. It is extremely important to note that the increased gift tax exemption is scheduled to expire on 12/31/2025. After this date, the exclusion will revert to its 2018 amount of $5 million adjusted for inflation. This limited window makes time of the essence and has made the SLAT a very powerful planning tool during this moment in time.

What's on Your Mind?

Philip Bekmessian

Philip Bekmessian is a Senior Manager and a member of the Financial Services Group with over 10 years of public accounting experience.

Start a conversation with Philip