Managing Fraud Risk: Identifying and Preventing Corruption Schemes in Construction Companies

- Published

- Jan 15, 2010

- Share

Fraud in the Construction IndustryAttributed to ACFE – Association of Certified Fraud Examiners – 2008 Report to the Nation

About the ACFE Survey

- Report done every 2 years, initially done in 1996.

- Based on surveys of CFE’s on cases investigated and resolved.

- 2008 report based on 959 cases across the country.

- Most authoritative survey of its type

CFMA – Fraud in Construction: Occupational Fraud

Definition: "The use of one's occupation for personal enrichment through the deliberate misuse or application of the employing organization's resources or assets"

Association of Certified Fraud Examiners – 2006 Report on Occupational Fraud and Abuse

Summary of Findings

- Occupational fraud schemes frequently continue for years before they are detected.

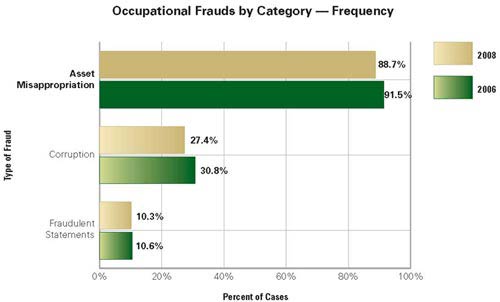

- Corruption is most common form of occupational fraud (27%), fraudulent billing schemes (24%) second.

- Data shows that fraud is more likely to be detected by a tip than by audits, controls, or any other means.

- Implementing major controls appears to reduce the median loss.

- Industries most vulnerable - Banking and Financial Services (15%), government (12%) and healthcare (8%).

- Small businesses are especially vulnerable to occupational fraud. Same for 2006 survey. Check tampering and fraudulent billing were the most common small business fraud schemes.

- Lack of adequate internal controls was most commonly cited

- Most victim companies modified their internal controls AFTER discovering they have been defrauded.

- Occupational frauds were most often committed by the accounting department or upper management.

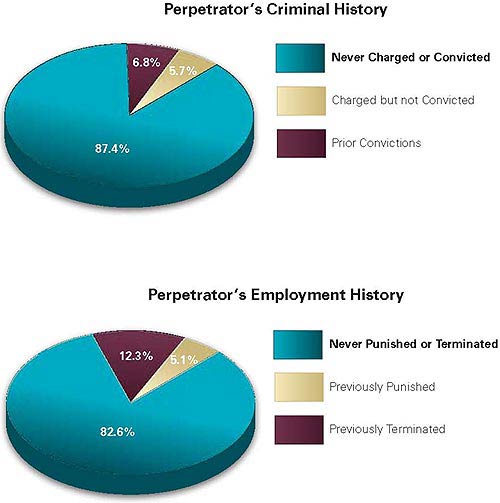

- Fraudsters are generally first-time offenders. Triangle of Opportunity, Incentive, Rationalization.

| CFMA – Fraud in Construction Occupational Fraud |

||

| Corruption | Asset Misappropriation | Fraudulent Statements |

| Conflicts of Interest • Purchasing Schemes • Sales Schemes Bribery • Invoice Kickbacks • Bid Rigging Illegal Gratuities Economic Extortion |

Cash • Larceny • Fraudulent Disbursements • Skimming Non Cash • Misuse • Asset Requisitions / Transfers • False Sales / Shipping • Purchases / Receiving |

Financial • Asset / Revenue overstatement / understatement • Timing differences • Fictitious Revenues • Concealed liabilities and expenses • Improper Disclosures • Improper Asset Valuations Non Financial • Employment Credentials • Internal and External Documents |

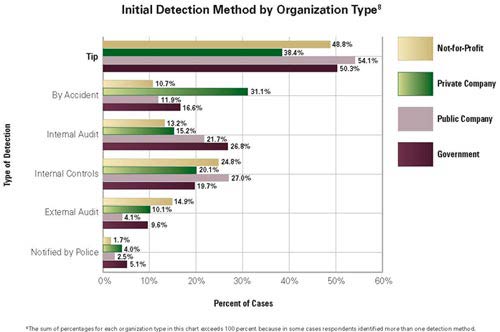

Detection of Fraud Schemes

- TIP or COMPLAINT - Nearly half of cases in 2008 study were uncovered by a tip or a complaint from an employee, customer, vendor, or other source.

- INTERNAL CONTROLS AND INTERNAL AUDITS

- Most helpful in government and public companies

- DISCOVERY BY ACCIDENT

- Most common in private companies

- EXTERNAL AUDIT

- Most helpful for private companies

TIPS

Greatest source of tips is from other employees

- Employees should be trained to understand fraud and how it harms the organization

- Encourage employees to report illegal or suspicious behavior

- Reassure employees that reports may be made confidentially and the organization prohibits retaliation against whistleblowers

30% of Tips came from external sources – encourage customers / vendors / stakeholders to report improper conduct

Small Businesses

- Business with less than 100 employees generally have fewer or weaker controls in place, primarily due to lack of personnel

- Small business frauds are more likely to be detected by tip or accident

- Room for improvement in their proactive detection efforts.

CFMA – Fraud in Construction

Occupational Fraud

Definition: "The use of one's occupation for personal enrichment through the deliberate misuse or application of the employing organization's resources or assets" Association of Certified Fraud Examiners – 2006 Report on Occupational Fraud and Abuse

Possible perpetrators

- Clerks

- Managers

- Executives

- Owners/Principals

Conclusion: Anyone in the company

Categories

- Misappropriating assets

- Corruption

- Falsifying financial statements

Is it fraud or abuse?

- Clandestine

- Fiduciary violation

- Committed to obtain financial benefit

- Costs company assets, revenues, or reserves

Why do employees commit fraud?

Cressy’s Fraud Triangle:

OpportunityIncentive

- Ability to commit fraud

- Get away with it

Rationalization

- Greed/desir

- Pressure/need

- Crucial element

- Justifies act

Observations

- Opportunity – Area where the employer has the most control

- Incentive – Employer cannot control but may be observable

- Rationalization – Grayest area; hardest for employer to discern

Categories

- Misappropriating assets

- Corruption

- Falsifying financial statements

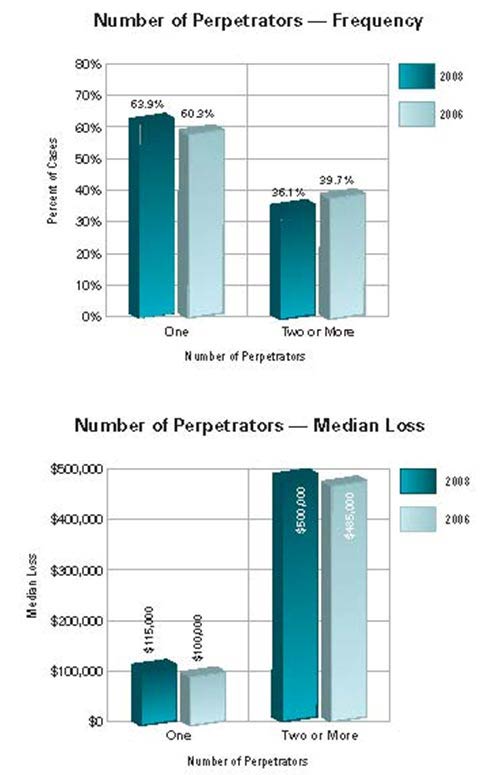

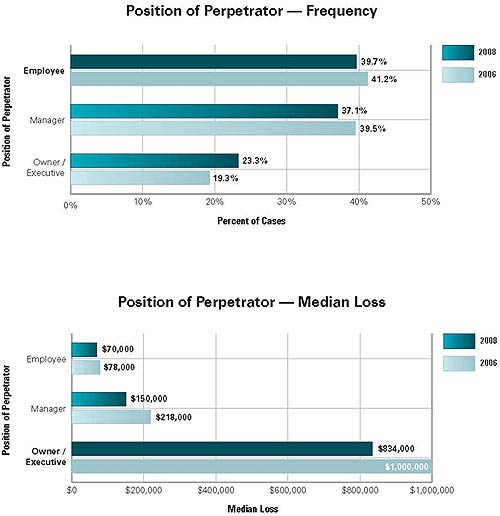

Frequency of Fraud Schemes:

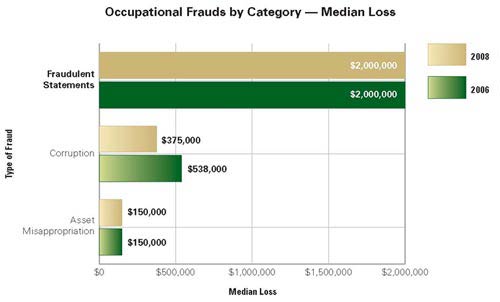

Occupational Fraud - Median Loss:

Corruption

Definition: Employee wrongfully influences a business transaction in order to procure some benefit for themselves or another person.

Categories

- Bribes

- Economic extortion

- Illegal gratuities

- Conflict of interest

Corruption - Bribes

Definition of Commercial Bribery: A business transaction where something of value is offered to influence a business decision.

- Differs from traditional bribery only in relation to what is being influenced.

Categories

- Kickbacks – Undisclosed payments made by vendors to employees of purchasing companies

- Bid rigging – Employee fraudulently assists a vendor in winning a contract

Kickback scheme commonalities

- Involve collusion between an employee and an outside party (vendor)

- Normally attack the purchasing function

- Consequently, purchasing employees are usually involved

Kickback scheme examples

Diverting additional business to a vendor

- Market pricing (where’s the harm?)

- No market incentive re: price and quality

- Incentive to recoup kickback

- Usually turn into overbilling scheme

Overbilling

- Vendor submits inflated invoice

- Higher than market pricing

- Shipped less product or lower quality product

- Fictitious invoice

- Employee may or may not have approval authority

Kickback payments

- Always a two-sided transaction

- Cash for kickbacks usually diverted to "slush fund"

- Non-company account

- Company checks to fictitious entity

- Paying false invoices

- Payments often charged as “fees” for consulting or other services

Bid rigging — In the context of bribes, bid rigging involves and illegal payment to an employee to assist a vendor in winning a contract.

- Employee fraudulently assists a vendor in winning a contract

- Subverts the bidding process

- Victim company’s employee tends to have influence in or access to bidding process

- High stakes in construction market (particularly in bad economic times)

Bid rigging categories:

Presolicitation phase

- Needs recognition schemes

- Specification schemes

- Tailoring/narrowing

- Prequalification requirements

- Vague specifications

- Bid splitting

- Advance look

Solicitation phase

- Bid rotation

- Fictitious suppliers

- Restricted bid period

Submission phase

- Abuse of sealed bid process

- Advance or inside information

Corruption – Economic Extortion

- Flip side of bribery scheme

- Employee demands payment to select vendor

- Pay up or else

- Transactionally the same as a bribe

Corruption — Illegal Gratuity — A gift given by a party who benefitted from a decision to the person who made the decision.

- Similar to bribe, but usually occurs after decision

- Often morph into bribery schemes

- May be a way to determine openness to a bribe

Generally follow a pattern

- Gifts, travel & entertainment

- Construction work, new windows, finished basement

- Cash

- Checks/financial instruments

- Hidden interests

- Loans

- Asset leases/sales below market

- Promises of favorable treatment

Corruption — Conflicts of Interest — Situations where an employee, manager, executive or partial owner has an undisclosed economic or personal interest in a transaction that adversely affects the company.

- May violate employee’s fiduciary duty owed to employer

- May violate terms of partnership, ownership or joint venture agreement terms

- Not all conflicts are economic

- Conflict vs bribery

- Approving fraudulent invoice for:

- Kickback, then its is bribery

- Fraudster’s company, then conflict of interest

- Transaction mechanics are the same

- Approving fraudulent invoice for:

Schemes

- Purchase schemes

- Inflated prices

- Rig bids

- False invoices

- Sales schemes

- Under-market pricing

- Write-off A/R

- Compete with employer

- Divert employer’s clients to employee’s company

- Unique assets transactions

- Usually involves land, buildings or large equipment

- Fraudster owns an interest in the asset

- Fraudster impacts negotiations in his favor

- Land flips

- Resource diversions

- Fraudster uses employer’s materials, equipment, or labor to assist his own company

Corruption — Detection

Most corruption schemes detected through:

- Tips from honest employees

- Tips from disgruntled co-workers

- Tips from disgruntled outsiders

- Tips from disgruntled co-conspirators

Tip allegations need to be validated through investigation

Red flags

- People

- Transactions

Red flags related to fraudsters

- Bribe takers/embezzlers

- Big spender

- Gift taker

- Odd couple

- Rule breaker

- Complainer

- Genuine need

- Bribe givers

- Gift bearer

- Sleaze factor

- Too-successful bidder

- Poor products or services

- One person operation

Red flags related to transactions

Purchasing

- Material reorder points routinely missed

- Use of same vendor(s)

- Purchasing policies not followed or consistently bent

- Analytics

- Pricing trends year to year or project to project

- Trends relative to market pricing

Bidding

- False statements in bid docs

- Sign-offs by unauthorized individuals

- Shortcutting or bypassing review proceduresv

- Bidders involved in developing bid docs

- Unusual variations in specification or contracts

- Short bid periods

- Vague terms in solicitation package

- Improper contact (business or social) with a bidder

- Acceptance of late bids/back dating of bids

- Changes to bid after all bids received (intentional errors)

- Patterns in bid awards

Analytics and corruption indicators

- Develop a body of historical data

- For each bid received

- For each bid awarded

- Actual costs for each contract

- By CIS number

- Cost/SQFT (installed)

- Unit prices

- Material prices by purchase unit

- Trend and compare historic data

- Year to year

- Project to project

- By sub/vendor

- By market

- By work (new, rehab, repair)

- By purchasing person

- Against competitors or industry metric

- Versus market pricing

- Look for departures from trends and anomalies

Conflicts of Interest

- Very difficult to uncover

- Discovery methods

- Tips

- Observation

- Analysis

Tips

- Other vendor complaints

- Employee complaints re: service or quality

Observation

- Lifestyles

- Financial problems

- Personal problems (divorce, addictions, relationships)

- Work habits (it takes time to run a side business)

- Involvement in areas of company outside of job duties

Analysis

- Periodic comparison of:

- Vendor and employee addresses

- Vendor TIN’s and employee SSN’s (including listed relatives

- Vendor phone numbers to all employee phone numbers

- Full investigation of vendor ownership done and filed with periodic reviews/updates

- Periodically interview purchasing employees to identify vendors receiving favorable treatment

- Credit and background checks

- Must have signed employee permission form on hand

- State laws vary, so review with counsel

Stimulus Monies — ARRA — American Recovery and Reinvestment Act of 2009

Purpose: Stimulate economy by accelerating "shovel ready" projects

Issues:

- Applies FAR to Stimulus projects

- Applies other Federal requirements to Stimulus projects

- NEPA compliance

- Buy American

- Whistleblower

- Federal fraud and false claims

- Contractor reporting

- Federal oversight

NEPA Compliance

- National Environmental Policy Act

- Required even if project has completed an environmental review

- NEPA compliance issues could create delays to construction start

- Adjust your schedules, budgets and/or estimates

- ARRA requires reviews to be "completed on an expeditious basis"

- Fed will likely use a streamlined process

- Even so, delay impacts should be planned for

Buy American

- Generally:

- All steel, iron and manufactured goods produced or manufactured in U.S.

- "Unmanufactured" construction material must be domestic (e.g. sand)

- All components or subcomponents of manufactured construction materials can be foreign

- Normally 50% must be domestic

- Contracting Officer must mark-up non-compliant bids by 25%

- Any waiver should (must) be obtained prior to submitting offer

Whistleblower Protection

- Applies to all "non-Federal" employees

- State & local governments, contractors and subs

- Offenses expanded from fraud to also include:

- Mismanagement, waste, abuse, substantial danger to public health, or violation of law or regulation

- Whistleblower must have only "reasonable belief"

- Employee has low burden to prove reprisal

- Employer must show “clear and convincing evidence” that action against employee would have occurred regardless of whistleblower status

- Economic times may cause employees blow whistle to avoid firing or layoff

Fraud and False Claims

- Legislation

- Passed into law

- Fraud Enforcement and Recovery Act (5/09) ("FERA")

- Pending

- H.R. 1788 False Claims Correction Act

- S. 458 False Claims Clarification Act

- vH.R. 1667 War Profiteering Prevention Act

- Passed into law

- FERA

- Protects TARP and other stimulus monies

- Authorizes funding to hire fraud prosecutors and investigators

- Extends False Claims Act to any false or fraudulent claim for government money or property whether or not:

- Claim is presented to government employee

- Government has physical custody of money

- Claimant intended to defraud the government

- Pending House and Senate bills

- Essentially apply FERA expansion of the FCA to all federal contracting

- War Profiteering Prevention Act

- Bill is still in Committee

- Aimed at U.S. companies with government contracts to provide goods and services overseas

- Establish criminal penalties for bid rigging, fraud, gross overcharging, delivery of faulty military parts, and environmental damage

Enhanced Quarterly Reporting

- Stimulus contracts in general require more extensive reporting and extend reporting to subs and material suppliers

- New FAR rule 52.204-11

- Applicable to any contract fully or partially ARRA funded

- Requires quarterly public on-line reporting of ARRA expenditures

- If prime or 1st tier sub, disclose names and total compensation of five highest-paid officers

- Reporting likely to be covered by FCA provisions

- Allows competitors access to ongoing projects’ cost and status

Enhanced Oversight

- Allows GAO access to prime and sub records

- Permits GAO to interview officers and employees of prime and subs

- IG powers expanded only to the prime contractor

- Contractors should:

- Increase internal and document controls

- Follow FAR to the letter

- Assure that consultants (CPA’s, attorneys and claims consultants) aware of changes to laws and regulations

- These new powers combined with new reporting means project performance issues need to be dealt with proactively

Contact EisnerAmper

Ready to take the next step? Share your information and we’ll reach out to discuss how we can help.