IRC Sec. 199A: Aggregation Election

- Published

- Sep 3, 2019

- Topics

- Share

Had William Shakespeare been around during the 2017 Tax Cuts and Jobs Act (“TCJA”), he would have proclaimed to his accountant: “To aggregate, or not to aggregate, that is the question.”

He would have also thought profoundly and at length whether or not his various business ventures are eligible for the IRC Sec. 199A aggregation election.

Executive Summary

Aggregation Tests: The regulations allow both individuals and relevant pass-through entities (“RPEs”) to aggregate provided they meet all five tests below:

- Control Test – Same person or group of persons, directly or indirectly by attribution under IRC Secs. 267(b) or 707(b), owns 50% or more of each trade or business to be aggregated.

- Majority Test – The control test above must exist for a majority of the tax year and be commonly controlled on the last day of the year.

- Same-Year Test – All of the items attributable to each trade or business must use the same tax year, not taking into account short tax years.

- Non-SSTB Test – None of the trades or businesses to be aggregated are Specified Service Trades or Businesses (“SSTBs”).

- Connection Test – Must satisfy at least two of the three factors below:

- Businesses provide products, property or services that are the same or customarily offered together.

- Businesses share facilities or significant centralized business elements (e.g., personnel, accounting, legal, manufacturing, purchasing, human resources or information technology).

- Businesses operate in coordination with, or reliance upon, one or more of the businesses in the aggregated group (e.g., supply chain interdependencies).

Key Terms and Reporting Requirements, cited below.

Shakespeare: Should I Aggregate My Businesses?

Accountant: It is usually more advantageous to aggregate; however, there are a few instances when it is less advantageous. For example, let’s suppose you have two businesses, one business has UBIA but no W-2 Wages; the second business has W-2 Wages, but no UBIA; and both businesses have QBI. In this situation, you will receive a greater deduction by not aggregating. Additionally, here are two examples in which you own three businesses. In both examples, you are married, have $300 million of taxable income (199A Deduction Cap is $60 million, or $300 million x 20%), and own 100% of each business (A, B, and C).

| Example 1 – More Advantageous “To Aggregate” | ||||

|---|---|---|---|---|

| A | B | C | Aggregate (A, B, and C) |

|

| QBI | 10,000,000 | 10,000,000 | 10,000,000 | 30,000,000 |

| W-2 Wages | 20,000,000 | None | 20,000,000 | 40,000,000 |

| UBIA | None | None | None | None |

| [A] QBI Limit: 20% of QBI |

2,000,000 | 2,000,000 | 2,000,000 | 6,000,000 |

| [B] Wage and UBIA Limit: (a) 50% of Wages |

10,000,000 |

None |

10,000,000 |

20,000,000 |

| (b) 25% of Wages + 2.5% UBIA | 5,000,000 | None | 5,000,000 | 10,000,000 |

| Greater Amount (a) or (b) | 10,000,000 | None | 10,000,000 | 20,000,000 |

| Tentative 199A Deduction: Lesser Amount [A] or [B] |

2,000,000 | None | 2,000,000 | 6,000,000 |

| Combined 199A Deduction</> | 4,000,000 | 6,000,000 | ||

Analysis: In Example 1, two businesses, A and C, have W-2 Wages; no businesses have UBIA; and the aggregate QBI limit of $6,000,000 is lower than the aggregate wage and UBIA limit of $20,000,000. It is more advantageous to aggregate, because business B is not able to utilize the 199A deduction since it has no W-2 Wages or UBIA.

| Example 2 – More Advantageous “Not to Aggregate” | ||||

|---|---|---|---|---|

| A | B | C | Aggregate (A, B, and C) |

|

| QBI | 100,000,000 | 100,000,000 | 100,000,000 | 300,000,000 |

| W-2 Wages | 20,000,000 | None | 20,000,000 | 40,000,000 |

| UBIA | None | 100,000,000 | None | 100,000,000 |

| [A] QBI Limit: 20% of QBI |

20,000,000 | 20,000,000 | 20,000,000 | 60,000,000 |

| [B] Wage and UBIA Limit: (a) 50% of Wages |

10,000,000 | None | 10,000,000 | 20,000,000 |

| (b) 25% of Wages + 2.5% UBIA | 5,000,000 | 2,500,000 | 5,000,000 | 12,500,000 |

| Greater Amount (a) or (b) | 10,000,000 | 2,500,000 | 10,000,000 | 20,000,000 |

| Tentative 199A Deduction: Lesser Amount [A] or [B] |

10,000,000 | 2,500,000 | 10,000,000 | 20,000,000 |

| Combined 199A Deduction | 22,500,000 | 20,000,000 | ||

Analysis: In Example 2, two businesses, A and C, have W-2 Wages; one business, B, has UBIA; and the aggregate QBI limit of $60,000,000 is greater than the aggregate wage and UBIA limit of $20,000,000. It is more advantageous not to aggregate, because business B is able to utilize $2,500,000 of the 199A deduction since it has UBIA.

In deciding whether or not to aggregate, the bottom line is you have to run the numbers.

Shakespeare: Are My Businesses Eligible for the Aggregation Election?

Accountant: If you have more than one business, the regulations allow you (or your RPE) to aggregate provided all five Aggregation Tests cited above are satisfied. You are not required to make the election, nor are you required to aggregate all of your businesses when making the election. In other words, you can pick and choose which businesses to aggregate and, as a result, it may increase your deduction. However, once you choose to aggregate two or more businesses, you must consistently report the aggregated businesses in all subsequent years. Summarized below are Aggregation Tests: (1) Control Test and (5) Connection Test, to assist you in determining your eligibility for the aggregation election.

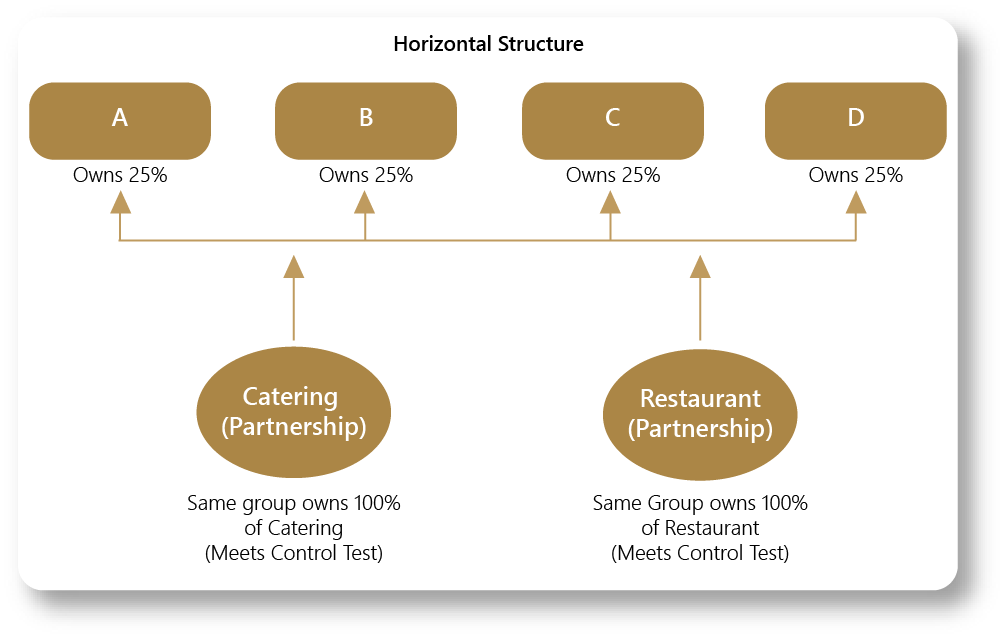

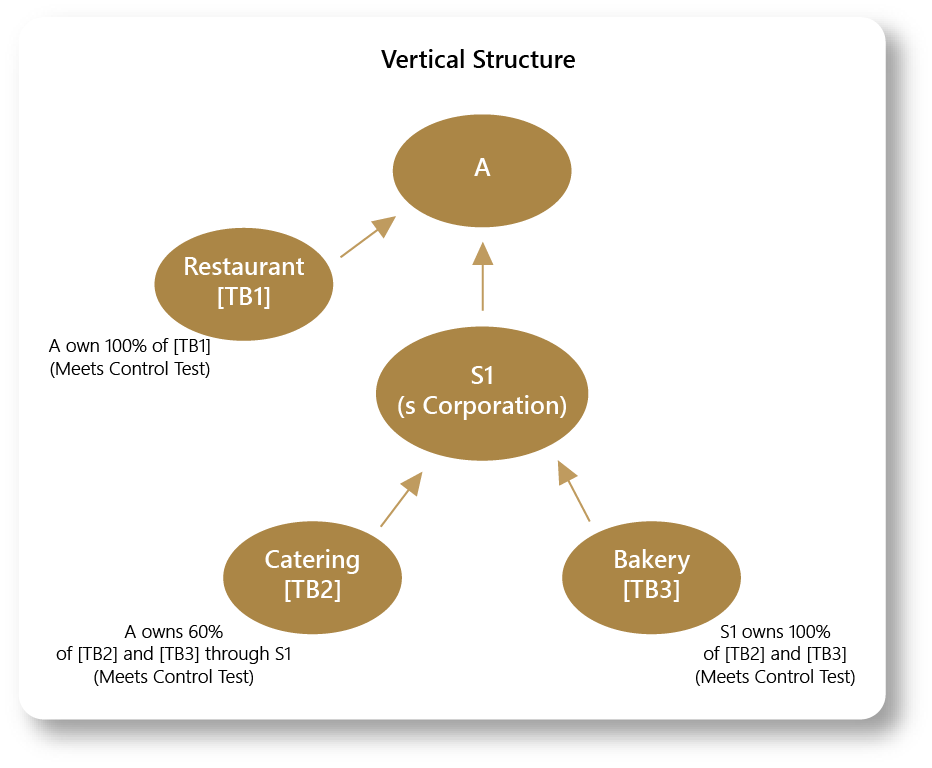

(1) Control Test: This test is defined as the same person or group of persons, directly or indirectly by attribution under IRC Secs. 267(b) or 707(b), owns 50% or more of each trade or business to be aggregated. For small business owners with either a horizontal or vertical business structure, this test is relatively easy to satisfy. See two examples below that demonstrate how the control test works.

Example 1 – Control Test:

Facts:

- A, B, C and D each own a 25% interest in each of two partnerships (a catering business and a restaurant).

- A, B, C and D are unrelated.

- Aggregation Tests: (2), (3), (4) and (5) are satisfied.

Analysis:

- Each owner may choose to treat the catering business and the restaurant as a single trade or business on their respective tax returns, because A, B, C, and D together own more than 50% of each of the two partnerships. Let’s take this example one step further and suppose each owner holds a 25% interest in each of ten partnerships. Each owner could then pick and choose any combination of the ten businesses they want to aggregate because the same group of persons owns more than 50% of each trade of business.

Example 2 – Control Test:

Facts:

- A directly operates a restaurant [TB1] and owns 60% of S1.

- S1, an S corporation, directly operates a catering business [TB2] and a bakery [TB3].

- Aggregation Tests: (2), (3), (4) and (5) are satisfied.

Analysis:

- There are two possible outcomes: (1) If S1 does not aggregate [TB2] with [TB3], A may aggregate [TB1] with any combination of [TB2] and [TB3]; (2) If S1 does aggregate [TB2] with [TB3], A may aggregate [TB1] with S1’s [Aggregated Trade or Business].

(5) Connection Test: This test requires that you satisfy at least two of the three factors below:

- Businesses provide products, property or services that are the same or customarily offered together.

- Businesses share facilitates or significant centralized business elements (e.g., personnel, accounting, legal, manufacturing, purchasing, human resources or information technology).

- Businesses operate in coordination with, or reliance upon, one or more of the businesses in the aggregated group (e.g., supply chain interdependencies).

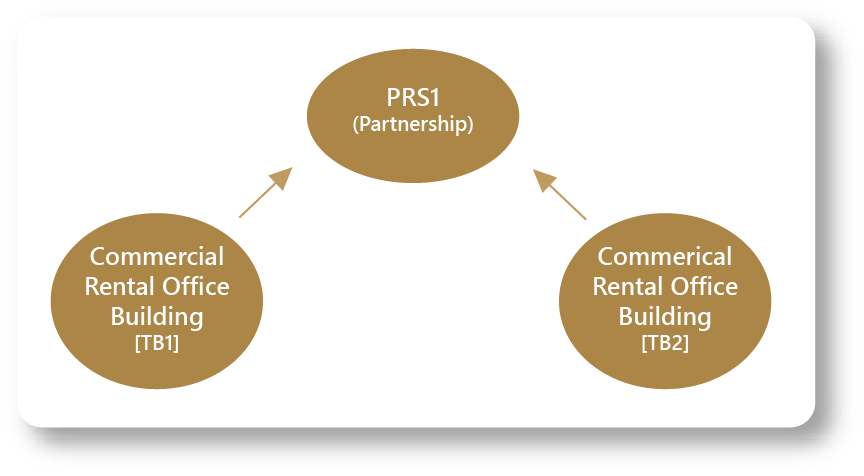

See two examples below that demonstrate how the connection test works.

Example 1 – Connection Test:

Facts:

- PRS1, a partnership, owns a commercial rental office building in state A [TB1] and a commercial rental office building in state B [TB2].

- [TB1] and [TB2] share centralized accounting, legal, and human resource functions.

- Aggregation Tests: (1), (2), (3) and (4) are satisfied.

Analysis:

- PRS1 may aggregate the two commercial buildings [TB1] and [TB2] into one trade or business because they are the same type of property (satisfies factor 1) and share centralized business elements (satisfies factor 2).

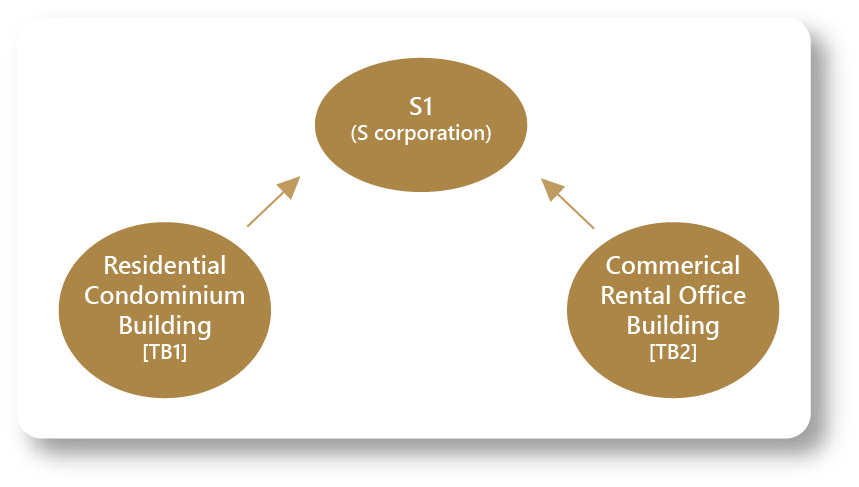

Example 2 – Connection Test:

Facts:

- S1, an S corporation, owns 100% of an interest in a residential condominium building in state A [TB1] and 100% of a commercial rental office building in state B [TB2].

- [TB1] and [TB2] share centralized accounting, legal, and human resource functions.

- Aggregation Tests: (1), (2), (3) and (4) are satisfied.

Analysis:

- S1 must treat the residential building [TB1] and commercial building [TB2] as separate trades or businesses. Although [TB1] and [TB2] share significant centralized business elements (satisfies factor 2), the two buildings are not the same type of property (fails factor 1), nor do they operate in coordination with, or reliance upon, one another (fails factor 3).

If you have a more complicated business structure, it is imperative that you contact your business advisory team for a full analysis.

Key Terms:

- Individual – Means an individual, trust (other than a grantor trust) or an estate.

- Relevant Pass-Through Entity (“RPE”) – Means a partnership (other than a publicly traded partnership) or an S corporation that is owned, directly or indirectly, by at least one individual,

estate or trust. A trust or estate is treated as an RPE to the extent it passes through QBI, wages or UBIA. - Qualified Business Income (“QBI”) – Net amount of qualified items of income, gain, deduction and loss with respect to any trade or business (or aggregated trade or business).

- QBI limit – Means 20% of taxpayer’s QBI.

- W-2 Wages and Unadjusted Basis Immediately After Acquisition (“UBIA”) Limit – Means the greater of 50% of the W-2 Wages, or the sum of 25% of the W-2 Wages plus 2.5% of the UBIA.

- Taxable Income Limit (“199A Deduction Cap”) – The 199A deduction is capped at 20% of the

amount by which the individual’s taxable income exceeds net capital gain.

Reporting Requirements:

- Consistency – Once you choose to aggregate two or more trades or businesses, you must consistently report the aggregated trades or businesses in all subsequent years. The aggregation

is irrevocable unless there is a material change in the facts and circumstances. - Disclosure Statement – Each year, you must attach a statement that includes the following:

- A description of each trade or business.

- The name and EIN of each entity in which a trade or business is operated.

- Information identifying any trade or business that was formed, ceased operations, or acquired or disposed of during the tax year.

- New Trade or Business – You may add a newly created or acquired trade or business to an existing aggregated trade or business if they meet all five Aggregation Tests cited above.

- 2018 Tax Year – For the 2018 tax year only, you can elect to aggregate on an amended return.

Contact EisnerAmper

Ready to take the next step? Share your information and we’ll reach out to discuss how we can help.