Making Repairs Work for You

- Published

- Dec 15, 2020

- Share

“Can’t I just expense everything anyway?”

In the last two-and-a-half years, since the Tax Cuts and Jobs Act (“TCJA”) was passed, this may have been the most popular question when it comes to capital expenditures (“CapEx”) and tax. With 100% bonus depreciation and increased IRC Sec. 179 expensing1 limits and eligibility, why not just capitalize and then expense everything?

Three reasons:2

- Due to state tax non-conformity, businesses leave money on the table by relying exclusively on bonus depreciation or IRC Sec. 179 expensing.

- Not all capital expenditures are eligible for bonus depreciation or IRC Sec. 179 expensing.

- A cost treated as a repair expense instead of a depreciable asset avoids depreciation recapture upon the sale of the property.

State Tax Issues

This chart summarizes state tax rates for three popular states and whether they conform to federal bonus depreciation and IRC Sec. 179 expensing.

|

State |

Corp. Tax Rate |

IRC Sec. Expensing |

Bonus Depreciation |

|---|---|---|---|

|

California |

8.84%3 |

Yes, but expensing limited to $25,000 with $200,000 investment limitation4 |

No bonus5 |

|

Michigan |

6.00%6 |

Conforms7 |

No bonus8 |

|

New York |

6.50%9 |

Generally conforms10 |

No bonus11 |

Consider two examples. In the first, the business ignores the state tax implications. It capitalizes everything and uses bonus depreciation. In the second example, the taxpayer applies the “repair regulations”12 to identify some of its “capital” expenditures as 100% deductible repairs.13

Example 1

If a Michigan corporation capitalizes $10 million as qualified improvement property (“QIP”) and deducts it using 100% bonus depreciation, the business will save $2.1 million on their federal income tax return. Since Michigan generally conforms to the federal tax code on a rolling basis, but does not conform to bonus depreciation, the corporation will be limited to a depreciation deduction of 3.33% (for 15-year QIP using the straight-line method and the half-year convention). The same $10 million will result in tax savings of $19,980.

|

Type of Deduction |

Basis |

Deprec. Rate |

Deduction |

Corp. Tax Rate |

Tax Savings |

|---|---|---|---|---|---|

|

Federal |

$10,000,000 |

100% |

$10,000,000 |

21.00% |

$2,100,000 |

|

State |

$10,000,000 |

3.33%14 |

$333,000 |

6.00% |

$19,980 |

|

|

|

|

|

Total |

$2,119,980 |

Example 2

The same Michigan corporation spends $10 million on possibly capital expenditures. Working with its tax advisors, the corporation identifies $5 million of the costs as repairs. The federal tax savings do not change; the corporation deducts $5 million in repairs and $5 million of bonus depreciation for federal tax savings of $2.1 million. Since Michigan conforms to the federal treatment of repairs, for state purposes the corporation will have a $5 million repair deduction and a $166,500 state depreciation deduction, resulting in state tax savings of $309,990. Applying the repair regulations saved the business an additional $290,010 in taxes in the first year, when compared with Example 1.

|

Type of Deduction |

Basis |

Deprec. Rate |

Deduction |

Corp. Tax Rate |

Tax Savings |

|---|---|---|---|---|---|

|

Federal Asset |

$5,000,000 |

100% |

$5,000,000 |

21.00% |

$1,050,000 |

|

Federal Repair |

N/A |

N/A |

$5,000,000 |

21.00% |

$1,050,000 |

|

State Asset |

$5,000,000 |

3.33%15 |

$166,500 |

6.00% |

$9,990 |

|

State Repair |

N/A |

N/A |

$5,000,000 |

6.00% |

$300,000 |

|

|

|

|

|

Total |

$2,409,990 |

When looking at these examples, please keep in mind that if the Michigan corporation had spent $1 million instead of $10 million, it could have used IRC Sec. 179 to expense the entire cost for both federal and state purposes. A California corporation, on the other hand, would be limited to expensing $25,000 under IRC Sec. 179 and could spend no more than $400,000 on IRC Sec. 179 property to claim an IRC Sec. 179 expensing deduction.

Ineligible Property

Not all improvements qualify for IRC Sec. 179 expensing or as QIP for bonus depreciation purposes. QIP is limited to interior improvements to a commercial building and excludes building expansions and costs related to elevators, escalators, or the interior structural framework of the building.16 IRC Sec. 179 includes more qualified real property improvements, such as roofs, HVAC, security systems, fire protection and alarm systems, and QIP.17 This still excludes many common improvements, such as exterior doors, windows, parking lots, or sidewalks. By analyzing these “improvements” through the lens of the repair regulations, businesses can find additional opportunities to expense repairs. Even if not all costs can be expensed as a repair, smaller businesses can use repair analyses to free up room under the IRC Sec. 179 expensing limit, which reduces the available IRC Sec. 179 expensing deduction.

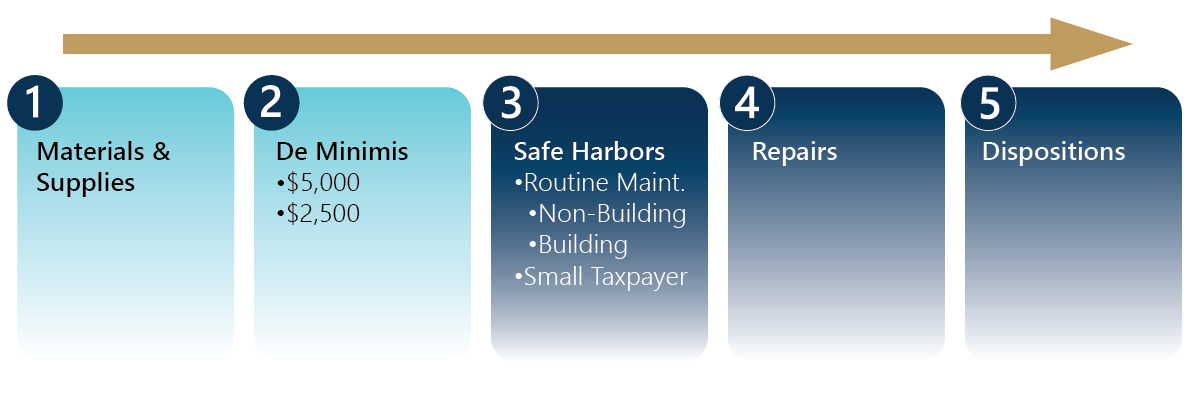

TPR Layers of Opportunity

The Repair Regulations18 have five different layers of opportunity summarized in this chart. Of those, the (3) Safe Harbors, (4) Repairs and (5) Dispositions are frequently included in cost segregation studies.

- Materials & Supplies – At each step, look at whether a cost is for materials or supplies that can be deducted immediately or when the material or supply is used.

- De Minimis – If the business has an accounting procedure or written policy under which assets or improvements with “de minimis” costs are expensed, they can make an election to follow this policy for tax purposes. This is a safe harbor limited to items under $5,000, if the taxpayer has an “applicable financial statement”;19 or, under $2,500, if it does not have an applicable financial statement.

- Safe Harbors – If the costs are greater than de minimis, see whether a safe harbor applies that would permit expensing. For example, there is a routine maintenance safe harbor for buildings that permits the expensing of damaged or worn parts that are routinely tested and replaced more than once during the ten-year period after the building is placed in service.

- Repairs – If none of these apply, see whether the costs are a repair.

- Dispositions – If the costs still must be capitalized, see whether they qualify for bonus depreciation or IRC Sec. 179 expensing while also seeing if an old asset was demolished as part of the improvement. In that case, you can take a disposition loss for the old asset.

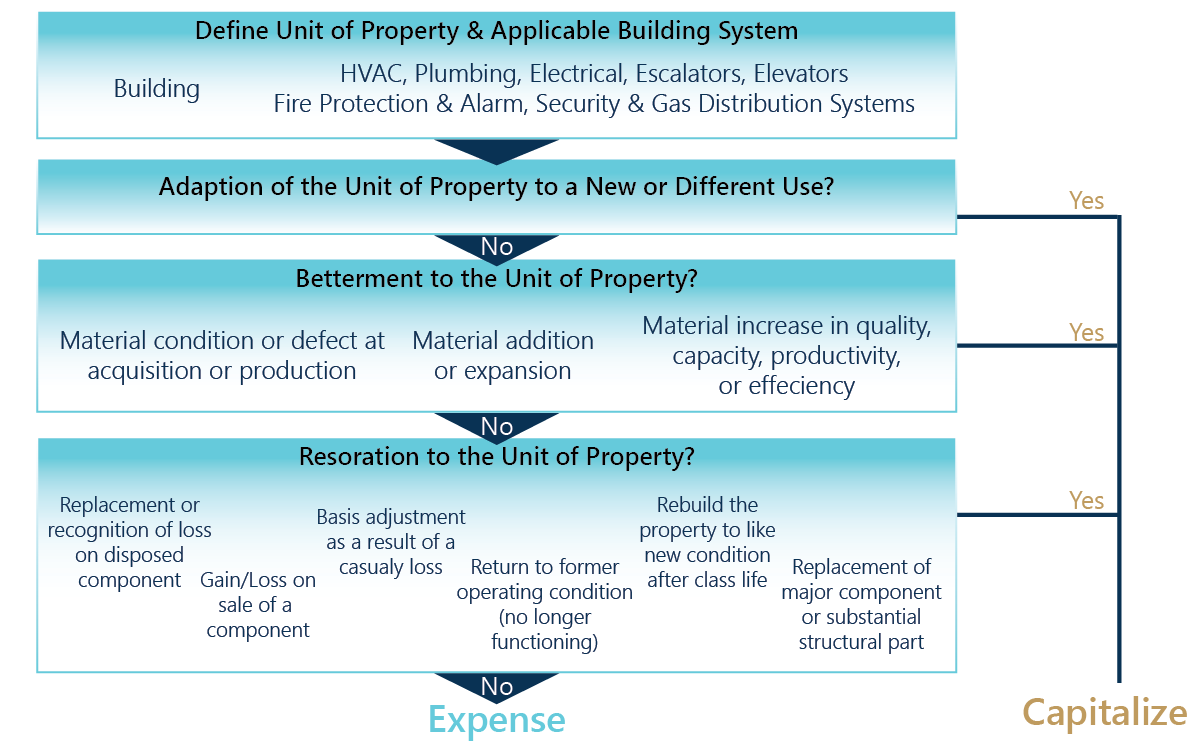

Repairs

This chart summarizes how to apply the ten tests20 to determine whether a cost is a repair or an improvement. Start with identifying a unit of property, (“UoP”) such as a building for a roof replacement. Then ask if the new roof adapts the building to a new or different use, which is most likely not the case. Then ask whether it is a “betterment.” With roofs, this could be the case if, for example, the replacement corrected a building defect. If the replacement was not a betterment, consider whether it was a restoration. For example, if the roofing system’s membrane was replaced, but nothing else, it would be a deductible repair. If the entire roof decking, coverings, and asphalt, and insulation, on the other hand, were replaced, this would be capitalized as the replacement of a major component or substantial structural part of the building. To sum it up, if an activity fails any of these ten tests, it is capitalized.

This next chart lists the seven building systems and their major components. It also lists the overall building UoP and provides examples of its components. When applying the tests in the above flow chart, each building system OR the overall building is analyzed as the UoP. The unit of property is important because it forms the basis for making comparisons. For example, when part of a roof is replaced, look at the overall building to see if a significant structural part of the building was restored. Another example would be looking at just the HVAC system when analyzing whether a new compressor is a betterment.

|

Systems |

Major Components of Building Systems |

|---|---|

|

HVAC |

Air handling units, boilers, condensing units, fans, furnaces, heat exchangers, heat pumps, make-up air units, refrigeration compressors, water chillers, etc. |

|

Plumbing |

Bathtubs, piping, pumps, sinks, toilets, urinals, water heaters, etc. |

|

Electrical |

Generators, light fixtures, panel boards, safety switches, switchboards, transformers, etc. |

|

Elevators & Escalators |

All elevators & escalators |

|

Fire Protection & Alarm |

Alarms, emergency exit signs & lights, heat & smoke detection devices, sprinkler heads & mains, water piping, etc. |

|

Security (Building) |

Alarm systems, electronic access systems, locks, monitoring devices such as cameras, etc. |

|

Gas Distribution |

Meters & gas distribution pipes |

|

Structure (Building UoP) |

Building components not included in other building systems. Examples are doors, windows, roof, ceilings, etc.… and structural components |

The following three examples show a repair analysis for HVAC air handling units (“AHUs”) with an emphasis on the question of restorations and whether the taxpayer is replacing a major component or substantial structural part of a building system or unit of property.

Example 3

| Assumptions: | Results: | Rooftop: |

|---|---|---|

|

Single Building

|

|

|

Example 4

| Assumptions: | Results: | Rooftop: |

|---|---|---|

|

Single Building

|

|

|

Example 5

| Assumptions: | Results: | Rooftop: |

|---|---|---|

|

Building 1

|

Building 1

|

|

|

Building 2

|

Building 2

|

|

The determination of whether costs can be expensed as a repair may be time-intensive, but it can result in large tax savings, especially for state tax purposes.

1 Under IRC Sec. 179, taxpayers may elect to deduct (or ‘‘expense’’) the cost of qualifying property, rather than to recover the cost through depreciation deductions.

2 There is a fourth reason. Technically speaking, capitalization is not a choice. At best, a taxpayer can make an election to capitalize repairs and maintenance to follow financial or book capitalization.

3 Cal. Rev. & Tax. Cd. § 23151(f)(1).

4 Cal. Rev. & Tax. Cd. § 24356.

5 Cal. Rev. & Tax. Cd. § 24349.

6 Mich. Comp. Laws Ann. § 206.623(1).

7 Mich. Comp. Laws Ann. § 206.607(1).

8 Mich. Comp. Laws Ann. § 206.607(1).

9 NY Tax Law § 210(1)(a). New York State also has a 29.4% MTA surcharge for Article 9-A taxpayers filing 2020 NYS corporation tax returns and doing business in the Metropolitan Commuter Transportation District (“MCTD”).

10 NY Tax Law § 208(9)(b)(16).

11 NY Tax Law § 208(9)(b)(17).

12 See generally T.D. 9636 as amended by T.D. 9689.

14 Depreciation rate of 3.33% is from Table A-8 of Publication 946 for the first year of 15-year QIP using straight-line depreciation with the half-year convention.

15 Depreciation rate of 3.33% is from Table A-8 of Publication 946 for the first year of 15-year QIP using straight-line depreciation with the half-year convention.

18 See Treas. Reg. § 1.263(a)-3.

19 An applicable financial statement generally means audited financial statements.

20 See Treas. Reg. § 1.263(a)-3. The ten tests for improvements are: (1) ameliorating a pre-existing condition or defect; (2) a material addition to, or material increase in the capacity of a unit of property ; (3) a material increase in the productivity, efficiency, strength, quality, or output of a UoP; (4) a replacement of a component of UoP for which a loss deduction was claimed (other than a casualty loss); (5) adaptation to a new or different use; (6) a replacement of a component of a UoP for which the adjusted basis was taken into account in computing loss or gain following a sale or exchange of the component; (7) a restoration of a UoP for which there was a basis adjustment on account of a casualty loss; (8) a return of the UoP to its ordinarily efficient operating condition after deterioration to the point where it is no longer functional for its intended purpose; (9) a rebuilding of the UoP to a like-new condition after the end of its class life; and, (10) a replacement of either a major component or a substantial structural part of a UoP.

Contact EisnerAmper

If you have any questions, we'd like to hear from you.

Receive the latest business insights, analysis, and perspectives from EisnerAmper professionals.