Quantifying Value Destruction in Regional Malls

- Published

- Oct 27, 2021

- Topics

- Share

Retail property owners are celebrating recent increases in foot traffic and sales as consumers, cash in hand, head back to stores. Spending on most categories of goods is increasing, and in-store shopping has risen faster than online purchases in recent months. That improves the health of retail tenants and, by extension, property owners. But not all segments of the retail sector are performing equally. Many regional malls, which have been in a steady decline for decades, continue to struggle as shifts in consumer behavior, the increase in e-commerce, and the pandemic have together caused tenant bankruptcies and store closings. Recently, the significant impact of these trends on mall valuations has become more evident.

The underlying issue for the mall sector is that there are too many of them. As new malls were developed aging properties remained, and typically gravitated to lower-priced retailers. Over the last decade, purchasing power has shifted from the Baby Boomer generation to Millennials and Gen Z who often prefer experiential purchases over buying goods and expensive apparel, the core of mall offerings. The massive growth in online shopping during the same period hit owners hard as anchors and then in-line tenants pulled back and space went dark. To cope, many owners spent significant capital to reallocate portions of the mall from apparel to dining, only to be slammed by a pandemic that closed all the restaurants.

Given these headwinds, intuition tells us that the value of many malls is declining. One window into this trend is a data set compiled by Trepp on loans collateralized by malls in the commercial mortgage-backed securities (CMBS) market. The Trepp data includes 62 loans (one loan is backed by a portfolio of malls) where recent appraisals can be compared to the appraised value of the collateral at the time the loan was originated. New appraisals are typically procured when a loan is transferred to special servicing. Accordingly, this sample is biased toward the lesser-performing mall loans in the CMBS universe. However, over 50% of the loan sample are current or less than 30 days delinquent making the data more relevant to the overall sector. The sample is also instructive because it includes loans of all sizes (from $16.3 million to $1.4 billion) and broadly covers geographies with properties located in 32 of the 50 states. The loans were originated between November 2005 and June 2021.

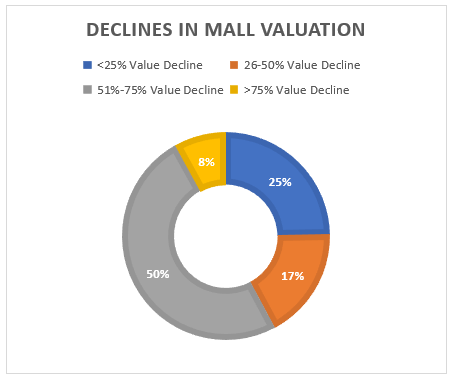

The aggregate value of the malls collateralizing the 62 loans at the time the loans were originated was $14.7 billion. The aggregate value of those malls based on the most recent appraisals (prepared between February 2019 and July 2021) was $7.4 billion. Accordingly, looking at the entire group of malls, on average the properties have lost half their value. The value loss on individual loans ranged from 8% to 91%, indicating that the events and circumstances of each property’s performance greatly influenced the magnitude of the lost value. As shown in the accompanying chart, stratifying the data set by the balance of the loan, the collateral securing 58% of the loans in the sample lost more than half of its value since the loan was made.

Source: Trepp sample of 62 CMBS regional mall loans.

Since most of the loans in the sample had been transferred to special servicing, stratifying the results by loan performance may determine whether these results reflect the mall sector more generally. Loans that were current, late but not yet delinquent, and performing but past their maturity dates make up over half of the total original appraised value of the sample. On average, the value of these malls declined 35% since origination indicating that even cash flowing centers have experienced significant deterioration of value. As expected, the decline was far greater for non-performing loans: On average, the value of malls collateralizing delinquent loans, including delinquent past maturity, declined 64%. For those loans in the process of foreclosure or already foreclosed, the value, on average, declined 73%.

Beyond declining net operating income, mall values are falling in the transactional market because there are fewer interested buyers. Many malls have high vacancies and require significant redevelopment, often into more productive uses. While there may be opportunities to create long-term value through re-tenanting, re-use, or developing new properties in a portion of the parking lot, these strategies require substantial capital. A new owner must also negotiate with existing tenants as well as community leaders whose constituents do not want to lose their place to gather and shop. As a result, the cap rate premium is necessarily higher on these properties, putting further downward pressure on values.

Malls aren’t going away. They continue to provide vital shopping and entertainment experiences to their communities. But we still have too many, and the transition to an appropriate store square footage to population ratio will continue to be a long and painful process. That process will necessarily result in continued loss of value for failing centers that require significant capital to reinvent the space.

Contact EisnerAmper

Ready to take the next step? Share your information and we’ll reach out to discuss how we can help.