Adoption of ASC 842, Leases, as Applied to Ground Leases

- Published

- Oct 11, 2021

- Share

Private real estate entities have had more than five years to prepare for the implementation of Topic 842, Leases, which is set to be effective for annual periods beginning after December 15, 2021, (January 1, 2022, for calendar-year reporting entities). While the lessor accounting remains largely unchanged, entities subject to a ground lease as a lessee will have fairly drastic changes to the existing accounting model.

The accounting for ground leases previously classified as operating leases is more complex under ASC 842, Leases. Here, we’ll provide an example of the implementation of ASC 842, Leases, on an existing ground lease as a lessee.

Practical Expedients

To make adoption easier, ASC 842 has provided for certain practical expedients. Among them is a package of three which must be elected together. An entity need not reassess:

- Whether any expired or existing contracts are or contain leases.

- The lease classification for any expired or existing leases.

- Initial direct costs for any existing leases.

Lease Classification

Under ASC 842, a ground lease can be classified as either an operating or finance lease. However, it also provides for a practical expedient whereby the lease classification under ASC 840 carries over.

If the practical expedient is not used, a lessee shall classify a lease as a finance lease when the lease meets any of the following criteria at lease commencement:

- The lease transfers ownership of the underlying asset to the lessee by the end of the lease term.

- The lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

- The lease term is for the major part of the remaining economic life of the underlying asset. However, if the commencement date falls at or near the end of the economic life of the underlying asset, this criterion shall not be used for purposes of classifying the lease.

- The present value of the sum of the lease payments and any residual value guaranteed by the lessee that is not already reflected in the lease payments in accordance with paragraph 842-10-30-5(f) equals or exceeds substantially all of the fair value of the underlying asset.

- The underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term.

When none of the criteria above are met, a lessee shall classify the lease as an operating lease.

Lessee Accounting: Impact on Balance Sheet and Income Statement

Under ASC 842, Leases, ground leases will be capitalized to the balance sheet through a “right-of-use asset” and lease obligation. The initial recognition and subsequent measurement will depend on the lease classification.

For finance leases, a lessee is required to do the following at adoption date:

- Recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in the statement of financial position.

- Recognize interest on the lease liability separately from amortization of the right-of-use asset in the income statement.

- Classify repayments of the principal portion of the lease liability within financing activities and payments of interest on the lease liability and variable lease payments within operating activities in the statement of cash flows.

For operating leases, a lessee is required to do the following at adoption date:

- Recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in the statement of financial position.

- Recognize a single-lease cost, calculated so that the cost of the lease is allocated over the lease term on a straight-line basis.

- Classify all cash payments within operating activities in the statement of cash flows.

If, under ASC 840, there is a cumulative effect of straight lining rents on the balance sheet at time of conversion, the balance should be netted with the new right-of-use asset.

Incremental Borrowing Rate

For many entities, the biggest hurdle in implementation will be the selection of the incremental borrowing rate. (After all, there is no market data for 99-year loans.) The determination of the incremental borrowing rate is an estimate that management needs to support.

Entities are required to select an appropriate rate that the lessee would pay to borrow on a collateralized basis over a similar term for an amount equal to the lease payments. A private company will typically need to find a reference borrowing using a comparable debt yield curve for its risk level and make adjustments for following differences:

- Secured Versus Unsecured: Adding collateral typically lowers the interest rate as the lender’s risk is reduced.

- Quality of Security: The more valuable the asset, the lower the risk to the lender, which could result in a lower rate.

- Guarantee: A loan guaranteed by the parent or owner has a lower risk to the lender, which could result in a lower rate.

- Payment Structure: How do the payment terms of the lease compare to the payment terms of reference borrowing? Generally, the later the principal is returned, the higher the risk to the lender such as an interest-only loan.

- Term: How does the lease term compare to the reference borrowing term? Longer terms typically increase the rate.

- Location: Rates can be affected by urban versus suburban, city to city, state to state, country to country.

- Time: Rates change over time as the economy changes.

- Credit Spread: How do the risk levels compare between the entity and the reference borrowing entity?

ASC 842, Leases, does not provide specific guidance for estimating the incremental borrow rate. As there are probably no exact matches to existing debt, this is an estimation. The following is one example but not necessarily the only method:

1. Find a base rate for secured borrowing that approximates the entity’s credit risk.

-

- Find a comparable corporate debt yield curve. Note, most corporate debt yields are unsecured.

- Consider what loan terms the entity could get if it was purchasing the asset (e.g., term, asset type, location).

2. Use the corporate debt yield curve to project the appropriate remaining life of the lease.

-

- How does the rate change from the reference borrowing of five or 10 years to 20 or 30 years? Use this curve to project the rate for the lease term, which could be more than 90 years.

3. Reconcile the reference borrowing rate to the concluded incremental borrowing rate.

-

- Adjust for differences such as secured versus unsecured, quality of security, payment structure, term location, time, credit spread.

The resulting incremental borrowing rate is supported with market data and can be applied to the lessee accounting.

Example

The following example serves to illustrate the concepts above. This is one interpretation and certainly not the only method to apply the guidance.

Summary of Facts

- The entity acquired the property on January 1, 20X1.

- The property is on a ground lease with the following terms:

- 97 years remaining at time of acquisition

- Fixed payments of $1,000,000 per year with 10% increases on 10-year anniversaries

- No renewal/termination/purchase option

- No transfer of ownership

- No residual value guarantee

- Initial direct costs of $150,000

- No cash incentive received

- Deferred straight-line rent liability under ASC 840 as of January 1, 20X2, is $584,107

- The lease was classified as an operating lease under ASC 840

- The entity entered into a mortgage on January 1, 20X1, with following terms:

- 2.75% interest rate

- Five-year term

- 80% LTV

- Secured by Class A office building in NYC

- The entity is adopting ASC 842 on January 1, 20X2.

Practical Expedients

The company has elected to use the practical expedient package to carryforward the operating classification from ASC 840 and carryforward previously capitalized initial direct costs under ASC 840.

Selection of Incremental Borrowing Rate

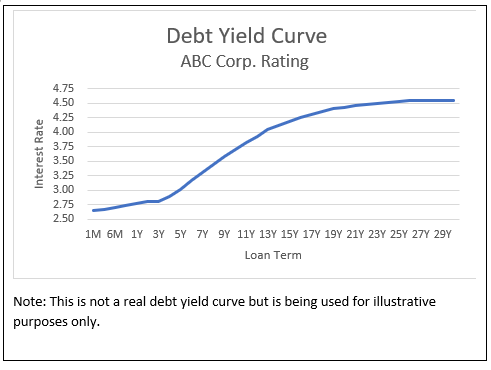

1. Find a reference borrowing rate using a comparable corporate debt yield curve.

The company has identified ABC Corp. to have similar credit rating. The following is its debt yield curve as of January 1, 20X2:

|

ABC Corp. Rating |

|

|---|---|

|

January 1, 20X2 |

|

|

Term |

Rate |

| 1M | 2.65 |

| 3M |

2.67 |

| 6M | 2.71 |

| 9M | 2.74 |

| 1Y |

2.77 |

| 2Y | 2.81 |

| 3Y | 2.81 |

| 4Y | 2.89 |

| 5Y | 3.02 |

| 6Y | 3.16 |

| 7Y | 3.31 |

| 8Y | 3.45 |

|

9Y |

3.58 |

| 10Y | 3.71 |

| 11Y | 3.82 |

| 12Y | 3.93 |

|

13Y |

4.04 |

| 14Y | 4.11 |

| 15Y | 4.18 |

| 16Y | 4.25 |

| 17Y | 4.31 |

| 18Y | 4.36 |

| 19Y | 4.41 |

| 20Y | 4.43 |

| 21Y | 4.46 |

| 22Y | 4.48 |

| 23Y | 4.50 |

| 24Y | 4.52 |

| 25Y | 4.53 |

| 26Y | 4.54 |

| 27Y | 4.54 |

| 28Y | 4.55 |

| 29Y | 4.55 |

| 30Y | 4.55 |

Based on the company’s existing loan terms, the five-year rate of ABC Corp. will be used as the reference borrowing.

2. Project spread to lease term.

Remaining lease term is 96 years. Following the debt yield curve of ABC Corp., the company estimates a 96-year term loan would have a rate of 4.58%.

| 96Y | 4.58% |

| 5Y | 3.02 |

| Spread | 1.56% |

3. Reconcile concluded incremental borrowing rate1.

| Reference Borrowing Rate | 3.02% |

| Adjustments: | |

|

Securitization |

(0.14) 0.05 (0.06) (0.08) (0.04) 1.56 |

| Incremental Borrowing Rate |

4.31% |

Initial Recognition

Lease Liability Calculation

| ASC 842 |

ASC 840 |

||||

|---|---|---|---|---|---|

| Cash Payments | Present Value | SLR Adjustment | Cumulative SLR | ||

| Year 1 | $1,000,000 | $958,681 | $584,107 | -$584,107 | |

| Date of Adoption | |||||

| Year 2 | 1,000,000 | 958,681 | 584,107 | (1,168,213) | |

| Year 3 | 1,000,000 | 919,069 | 584,107 | (1,752,320) | |

| Year 4 | 1,000,000 | 881,094 | 584,107 | (2,336,427) | |

| Year 5 | 1,000,000 | 844,688 | 584,107 | (2,920,534) | |

| ... | |||||

| Year 97 | 2,357,948 | 41,043 | (773,841) | (0) | |

| $152,658,351 | $27,876,006 | ||||

Right-of-Use Asset Calculation

| Lease Liability | $27,876,006 |

| SLR Liability | (584,107) |

| Right-of-Use Asset | $27,291,899 |

Journal Entries

| Account | Debit | Credit |

|---|---|---|

Right-of-Use Asset |

27,291,899 | |

| Deferred Straight-Line Rent Liability | 584,107 |

|

| Lease Liability | (27,876,006) |

Subsequent Measurement

Lease Liability

|

Beginning Balance A |

Liability Accretion B |

Lease Payment C |

Enging Balance A+B+C+D |

|

|---|---|---|---|---|

| Year 2 | 27,876,006 | 1,201,456 | (1,000,000) | 28,007,462 |

| Year 3 | 28,077,452 | 1,210,139 | (1,000,000) | 28,287,600 |

| Year 4 | 28,287,600 | 1,219,196 | (1,000,000) | 28,506,796 |

| Year 5 | 28,506,796 | 1,228,643 | (1,000,000) | 28,735,439 |

| ... | ||||

| Year 97 | 2,260,519 | 97,428 | (2,357,948) | 0 |

Right-of-Use Asset

|

Beginning Balance |

Lease Cost |

Liability Accretion G |

Ending Balance |

|

|---|---|---|---|---|

| Year 2 | 27,291,899 | (1,584,107) | 1,201,456 | 26,909,248 |

|

Year 3 |

26,909,248 | (1,584,107) |

1,210,139 | 26,535,280 |

|

Year 4 |

26,535,280 | (1,584,107) | 1,219,196 |

26,170,369 |

| Year 5 | 26,170,369 | (1,584,107) |

1,228,643 | 25,814,905 |

| ... | ||||

| Year 97 | 1,486,678 | (1,584,107) | 97,428 | 0 |

Journal Entries

| Account | Debit | Credit |

|---|---|---|

Lease Cost Expense (F) |

$1,584,107 | |

| Right-of-Use Asset (F+G) | -$382,651 |

|

| Lease Liability (B+C) | -$201,456 | |

| Cash (C) | -$1,000,000 |

With the implementation of ASC 842, Leases, right around the corner, real estate entities can take comfort knowing their lessor accounting has minimal impact. For those that are subject to a ground lease as a lessee, now is the time to be preparing for the implementation. Due to the complexities involved, consultation with an experienced real estate advisor is strongly recommended.

1All of these adjustments are fictitious amounts used for illustrative purposes only. Consult with an experienced valuation professional as to actual adjustments.

2Total cash payments over remaining lease term adjusted for deferred straight-line rent balance at time of adoption.

What's on Your Mind?

Paul Dolinshek

Paul Dolinshek is a Senior Manager in the Real Estate Services Group, with 10 years of public accounting experience serving the real estate and hospitality industry.

Start a conversation with Paul

Receive the latest business insights, analysis, and perspectives from EisnerAmper professionals.